10 Apr

The Bank of Canada held its overnight rate steady at 2.25% on March 18, 2026, yet fixed mortgage rates in Toronto climbed throughout April—some lenders now quoting 5.9% to 6.4% for self-employed borrowers and investors. This paradox defines the Toronto Mortgage Shake-Up April 2026: New Investor Rules, Rising Fixed Rates & Opportunities for First-Time Buyers and Self-Employed Borrowers, where regulatory changes and global bond market volatility are reshaping who can borrow, how much they can access, and what strategies work best in Canada’s largest real estate market.

April 2026 marks a turning point. New federal investor mortgage rules now prevent double-counting of personal income across multiple properties, fixed rates are rising due to geopolitical tensions driving bond yields higher, and Toronto’s elevated inventory is creating rare negotiating power for first-time buyers. Meanwhile, self-employed borrowers face a complex rate environment requiring proactive planning. Understanding these four interconnected dynamics is essential for anyone navigating Toronto’s mortgage market this spring.

Key Takeaways

✅ New investor rules introduced in Q1 2026 eliminate double-counting of income—each investment property must now qualify independently with its own debt service coverage and only 50-70% of rental income counts toward qualification.

✅ Fixed mortgage rates are climbing in April 2026 (5.9%-6.4% for self-employed borrowers) despite the Bank of Canada holding its overnight rate at 2.25%, driven by rising bond yields from geopolitical uncertainty and trade tensions.

✅ First-time buyers have leverage in Toronto’s current market with elevated inventory, easing prices, and combined land transfer tax rebates worth up to $8,475 ($4,000 Ontario + $4,475 Toronto).

✅ Self-employed borrowers need to act proactively—rates of 5.9%-6.4% in 2026 require strong documentation, lower debt ratios, and potentially exploring B-lenders or alternative solutions.

✅ Approximately one million Canadians are still facing significantly higher rates at renewal in 2026, making early planning and broker consultation critical.

Understanding the Toronto Mortgage Shake-Up April 2026: What’s Changed for Investors

The New IPRRE Classification and What It Means

The Office of the Superintendent of Financial Institutions (OSFI) introduced a new Income-Producing Residential Real Estate (IPRRE) classification effective in early 2026. This designation flags mortgages where repayment relies heavily on rental income as higher risk, requiring banks to hold more capital and apply significantly tighter qualification rules.

For Toronto real estate investors, this represents the most substantial regulatory shift in a decade. Here’s what changed:

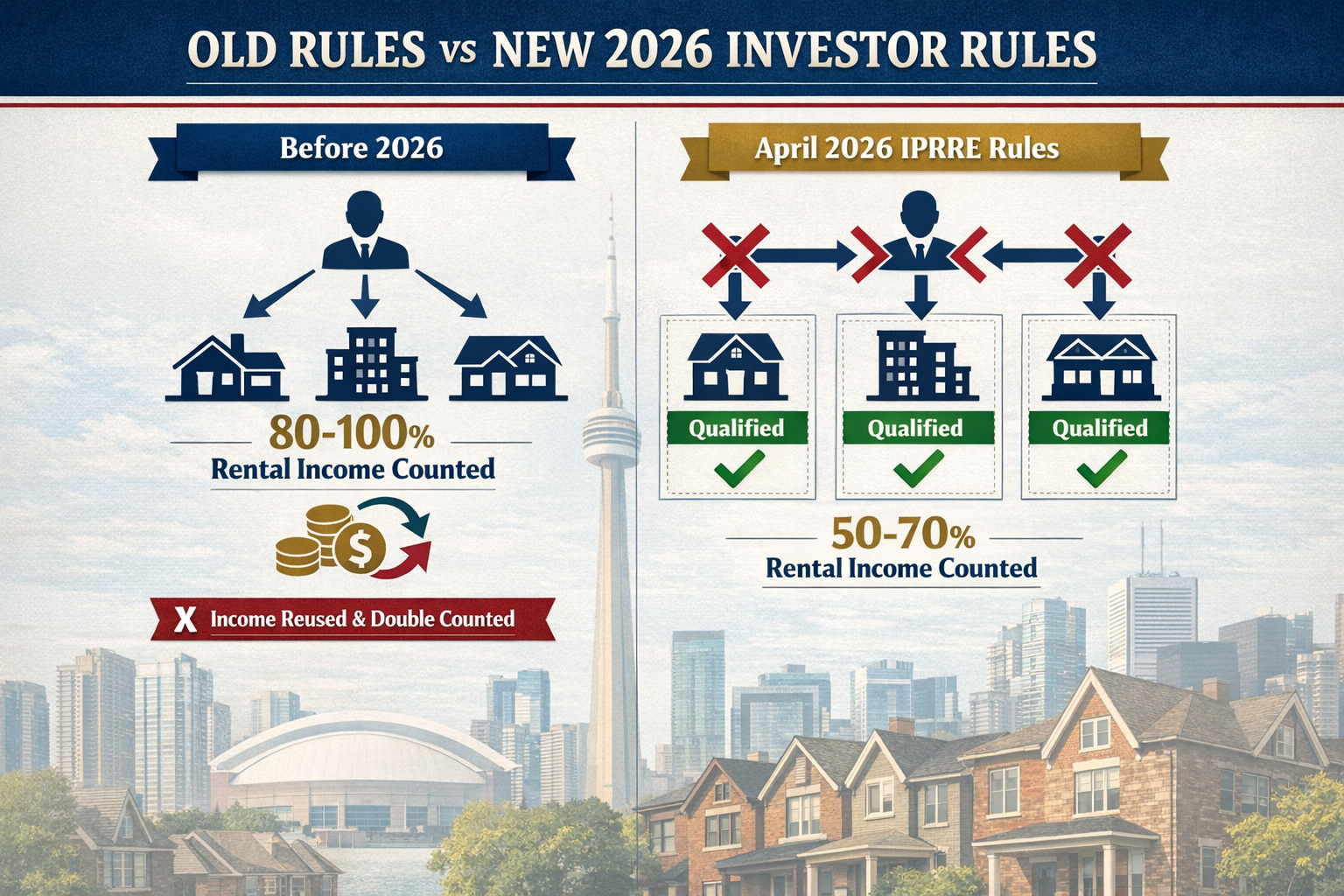

Before 2026:

- Lenders counted 80-100% of rental income toward mortgage qualification

- Investors could reuse the same personal income across multiple mortgage applications

- Portfolio scaling was relatively straightforward with strong personal income

April 2026 and Beyond:

- Lenders now count only 50-70% of rental income toward qualification

- No double-counting: Each property must qualify independently with its own debt service coverage

- Personal income cannot be reused across multiple simultaneous applications

- Refinancing and equity access depend on whether each property qualifies independently

Real-World Impact on Toronto Investors

Let’s look at a practical example. A Toronto investor with $150,000 annual personal income previously could use that same income to qualify for multiple properties, supplementing with 80-100% of projected rental income. Under the new rules:

- That $150,000 can only support one mortgage application at a time

- Rental income is discounted to 50-70% of actual or projected rent

- Each subsequent property must stand on its own rental income and debt service coverage

This dramatically reduces borrowing capacity for portfolio investors. A property generating $3,000 monthly rent ($36,000 annually) now contributes only $18,000-$25,200 toward qualification instead of $28,800-$36,000.

Toronto’s Multiplex Strategy: A Silver Lining

Toronto investors who followed a balanced investment model—combining strong personal income with rental income rather than maximizing leverage on day-one cash flow—are less affected. Properties that don’t rely primarily on rental income for debt service avoid IPRRE classification entirely.

This means Toronto’s traditional duplex, triplex, and fourplex strategies remain viable for investors with solid employment income who view rental income as supplementary rather than primary. The new rules hit hardest on investors who were stretching qualification by maximizing rental income assumptions.

Capital Gains Stability Amid Regulatory Change

One piece of good news: the capital gains inclusion rate for investors remains at 50% in 2026, providing some stability amid other regulatory tightening. This means the tax treatment of investment property sales hasn’t changed, even as qualification rules have tightened significantly.

For more insights on navigating investment properties as a self-employed individual, see our guide on investing in rental properties as a self-employed individual in Canada.

Rising Fixed Rates in April 2026: Why Rates Are Climbing Despite BoC Stability

The Bond Market Disconnect

Here’s the puzzle confusing many Toronto borrowers in April 2026: the Bank of Canada held its overnight rate at 2.25% on March 18, yet fixed mortgage rates have been climbing steadily. Self-employed borrowers are now seeing rates of 5.9% to 6.4%, and even prime borrowers are facing higher fixed rates than they did in February.

The answer lies in bond yields, not the overnight rate.

Fixed mortgage rates are priced off Government of Canada bond yields, particularly the 5-year bond. When bond yields rise, fixed mortgage rates follow—regardless of what the Bank of Canada does with its overnight rate (which primarily affects variable rates).

What’s Driving Bond Yields Higher?

Several factors are pushing Canadian bond yields upward in April 2026:

📈 Geopolitical tensions: Ongoing conflicts and trade uncertainty are creating volatility in global bond markets

📈 U.S. fiscal policy: Large deficits and debt concerns south of the border are putting upward pressure on North American yields

📈 Inflation concerns: While inflation has moderated, markets remain cautious about potential resurgence

📈 Global capital flows: Investors are demanding higher yields to hold Canadian government debt amid uncertainty

The result? Five-year Government of Canada bond yields have climbed approximately 40-60 basis points since early 2026, and lenders have passed those increases directly to borrowers through higher fixed mortgage rates.

Variable Rates: A Different Story

While fixed rates climb, variable rates remain relatively stable because they’re tied to the Bank of Canada’s overnight rate, which has held at 2.25%. This creates an interesting opportunity for borrowers comfortable with rate fluctuation.

Current variable rates for well-qualified borrowers are sitting around 3.45%-3.95%, significantly lower than fixed rates. For self-employed borrowers, variable rates through alternative lenders may be available at 4.5%-5.2%—still better than fixed options.

For a detailed comparison of fixed versus variable strategies, check out our analysis of fixed vs variable rates for Toronto first-time buyers.

What This Means for Your Mortgage Decision

The widening gap between fixed and variable rates creates a strategic decision point:

Choose Fixed If:

- You need payment certainty and can’t handle increases

- You believe rates will rise significantly in the next 2-3 years

- You’re stretching your budget and need predictability

Choose Variable If:

- You have payment flexibility and can absorb potential increases

- You believe the Bank of Canada will hold or cut rates in 2026-2027

- You want to benefit from the current 150-200 basis point discount versus fixed

Opportunities for First-Time Buyers in Toronto’s April 2026 Market

The Perfect Storm of Buyer Leverage

While investors face tighter rules and everyone confronts higher fixed rates, first-time buyers in Toronto are experiencing rare advantages in April 2026. Several factors have aligned to create genuine opportunities:

1. Elevated Inventory and Easing Prices

Toronto’s housing inventory has increased significantly compared to the tight market of 2021-2022. More listings mean:

- Less competition for entry-level condos, townhouses, and starter homes

- Negotiating power returning to buyers after years of seller dominance

- Price stability or modest declines in many segments, particularly condos

The new investor rules have reduced competition from portfolio buyers targeting entry-level properties, further tilting the balance toward owner-occupants.

2. Substantial Land Transfer Tax Rebates

First-time buyers in Toronto benefit from two stacked rebates that can save thousands:

💰 Ontario Land Transfer Tax Rebate: Up to $4,000 for first-time buyers

💰 Toronto Municipal Land Transfer Tax Rebate: Up to $4,475 for first-time buyers

Combined maximum rebate: $8,475

These rebates apply to the land transfer taxes you’d otherwise pay on closing. For a $700,000 condo, land transfer taxes would typically total approximately $17,000—but first-time buyers can reduce this by $8,475, bringing the actual cost down to roughly $8,525.

This is real money that can stay in your pocket or go toward furniture, renovations, or emergency savings.

For more details on first-time buyer programs and incentives, see our guide on navigating the first-time home buyer tax credit in Canada.

3. Increased Insured Mortgage Cap

Effective December 15, 2024, the insured mortgage cap increased from $1 million to $1.5 million, with down payment requirements of:

- 5% on the first $500,000

- 10% on the remainder

This change dramatically reduced barriers for mid-range home buyers. A $1.25 million home now requires only $100,000 down instead of the previous $250,000 (20% requirement for uninsured mortgages above $1 million).

This opens substantially more options for Toronto buyers previously priced out of detached and semi-detached markets, particularly in neighborhoods like North York, Scarborough, and Etobicoke.

4. Stress Test Changes on the Horizon

By mid-2026, OSFI is expected to remove the B20 mortgage stress test requirement for uninsured mortgages, replacing it with portfolio-level caps limiting the percentage of new loans each quarter that can exceed 450% of borrower income.

This change will:

- Increase borrowing capacity for many buyers

- Create more competition for lenders (easier to switch at renewal)

- Potentially push prices higher as qualification becomes easier

Strategic timing matters: Buyers who act in April-May 2026 may secure properties before these changes drive prices upward later in the year.

5. Condo Market Opportunities

Toronto’s condo market has been particularly affected by elevated inventory and reduced investor demand. This creates opportunities for first-time buyers who:

- Can negotiate price reductions or seller concessions

- Have access to units that would have faced bidding wars in 2021-2022

- Can secure favorable terms on pre-construction assignments

For insights specific to Toronto’s condo market, read our analysis of the rise of condo living in Toronto and what it means for first-time buyers.

Common First-Time Buyer Mistakes to Avoid

Even in a favorable market, first-time buyers can stumble. Watch out for:

❌ Maxing out your approval: Just because you’re approved for $800,000 doesn’t mean you should spend it all

❌ Ignoring closing costs: Budget 1.5-4% of purchase price for legal fees, land transfer taxes (after rebates), inspections, and moving

❌ Skipping pre-approval: Get pre-approved before house hunting to know your true budget and lock in a rate

❌ Overlooking condo fees and property taxes: These ongoing costs significantly impact affordability

For a comprehensive list, see our guide on first-time home buyer mistakes.

Self-Employed Borrowers: Navigating Higher Rates and Tighter Qualification in 2026

The Self-Employed Rate Reality

Self-employed and business-for-self borrowers face a more challenging mortgage environment in April 2026, with rates typically ranging from 5.9% to 6.4% for fixed mortgages and 4.5% to 5.5% for variable options through alternative lenders.

Why the premium? Lenders view self-employed income as higher risk due to:

- Income variability and business cycle sensitivity

- Tax write-offs that reduce reported income

- Less predictable cash flow compared to salaried employees

- Higher default rates historically (though this gap has narrowed)

Strategies to Secure Better Rates as a Self-Employed Borrower

The good news: proactive planning can significantly improve your rate and approval odds. Here’s what works in 2026:

1. Strengthen Your Documentation

Lenders want to see:

✅ Two years of complete tax returns (T1 Generals and Notices of Assessment)

✅ Business financial statements if incorporated

✅ Strong credit score (ideally 680+ for prime lenders, 600+ for alternatives)

✅ Consistent or growing income year-over-year

The more complete and professional your documentation, the better your rate. Consider working with an accountant to present your income in the most favorable light while remaining compliant.

2. Lower Your Debt Ratios

Self-employed borrowers benefit enormously from low debt-to-income ratios. Before applying:

- Pay down credit cards and lines of credit

- Avoid taking on new car loans or financing

- Consider paying off small debts entirely to improve ratios

Target keeping your Total Debt Service (TDS) ratio below 40% if possible—this opens doors to better lenders and rates.

3. Consider B-Lenders and Alternative Solutions

If prime lenders quote rates above 6%, explore B-lenders like:

- Home Trust

- MCAN

- MCAP

These lenders specialize in self-employed borrowers and may offer rates in the 3.7%-5.5% range depending on your profile, down payment, and property type.

For detailed rate comparisons, see our analysis of B-lender mortgage rates for self-employed Toronto borrowers.

4. Explore Bank Statement Programs

Some lenders offer bank statement mortgage programs that qualify you based on deposits rather than tax returns. This works well for borrowers who:

- Write off significant business expenses

- Have strong cash flow but lower reported income

- Can demonstrate consistent deposits over 12-24 months

Rates are typically higher (5.5%-6.5%), but approval odds improve dramatically.

Learn more about bank statement mortgages for self-employed borrowers.

5. Lock In Rates Early

With fixed rates climbing in April 2026, self-employed borrowers who delay may face even higher rates by summer. Consider:

- Getting pre-approved now to lock in current rates (typically holds 90-120 days)

- Working with a mortgage broker who can shop multiple lenders simultaneously

- Exploring rate-hold options if you’re 3-6 months from purchase

For timing strategies, read our guide on self-employed Toronto mortgages and locking rates before BoC stability ends.

Self-Employed Renewals: A Critical Consideration

Approximately one million Canadians are facing mortgage renewals in 2026 at significantly higher rates than their previous terms. Self-employed borrowers at renewal face unique challenges:

- Your income may have changed since your original approval

- New documentation requirements may apply

- Your current lender may not offer competitive rates

Don’t assume you must renew with your current lender. You have options:

✅ Shop competing lenders 4-6 months before renewal

✅ Consider switching to a variable rate if fixed rates are prohibitively high

✅ Explore refinancing to consolidate debt or access equity

For renewal-specific strategies, see our comprehensive guide on self-employed mortgage renewals in 2026.

Resources for Self-Employed Borrowers

The Everything Mortgages team has created extensive resources specifically for self-employed Canadians:

- Mortgages for Self-Employed Borrowers

- The Ultimate Guide to Securing a Mortgage for Self-Employed Canadians

- How Self-Employed Borrowers Can Secure Insurable Mortgage Rates in Toronto Under New 2026 Rules

- Self-Employed Mortgages for Contractors

Actionable Steps for Toronto Borrowers in April 2026

For Real Estate Investors

✅ Reassess your portfolio strategy under the new IPRRE rules—focus on properties that can qualify independently

✅ Strengthen rental income documentation with signed leases and rental history

✅ Consider refinancing existing properties before rules tighten further

✅ Explore multiplex strategies that combine personal income with rental income rather than relying primarily on cash flow

✅ Work with a mortgage broker experienced in investor mortgages and the new 2026 rules

For First-Time Buyers

✅ Take advantage of elevated inventory and negotiate aggressively—this is a buyer’s market

✅ Claim both land transfer tax rebates (Ontario + Toronto = up to $8,475)

✅ Get pre-approved early to lock in current rates before potential increases

✅ Consider variable rates if you have payment flexibility—they’re 150-200 basis points lower than fixed

✅ Budget conservatively for closing costs, condo fees, property taxes, and maintenance

✅ Avoid common mistakes by reviewing our first-time home buyer mistakes guide

For Self-Employed Borrowers

✅ Gather two years of complete tax documentation and business financials

✅ Lower debt ratios by paying down credit cards and avoiding new debt

✅ Explore B-lenders and alternative solutions if prime lenders quote rates above 6%

✅ Consider bank statement programs if you write off significant expenses

✅ Lock in rates early before further increases—get pre-approved now

✅ Review renewal options 4-6 months before your term ends

✅ Work with a broker specializing in self-employed mortgages who can access multiple lender options

For specialized guidance, see our resources on obtaining a mortgage when you’re self-employed and innovative mortgage solutions for self-employed Canadians.

The Role of Mortgage Brokers in Navigating the 2026 Shake-Up

Why Broker Expertise Matters More Than Ever

The Toronto Mortgage Shake-Up April 2026: New Investor Rules, Rising Fixed Rates & Opportunities for First-Time Buyers and Self-Employed Borrowers has created a complex landscape where one-size-fits-all advice no longer works.

Mortgage brokers provide:

🎯 Access to multiple lenders: Banks, credit unions, B-lenders, and private lenders—all with different criteria and rates

🎯 Specialized knowledge: Understanding which lenders work best for self-employed borrowers, investors under new rules, or first-time buyers

🎯 Rate shopping: Brokers can compare dozens of options simultaneously, saving you time and money

🎯 Application strategy: Knowing how to present your income, structure your application, and maximize approval odds

🎯 Ongoing support: From pre-approval through closing and future renewals

In April 2026, with new investor rules, climbing fixed rates, and varying qualification criteria across lenders, working with an experienced mortgage broker is more valuable than ever.

Conclusion: Navigating Toronto’s Mortgage Market in April 2026

The Toronto Mortgage Shake-Up April 2026: New Investor Rules, Rising Fixed Rates & Opportunities for First-Time Buyers and Self-Employed Borrowers represents a fundamental shift in Canada’s largest real estate market. New IPRRE investor rules have eliminated double-counting of income and reduced rental income qualification, fixed rates are climbing due to bond market volatility despite Bank of Canada stability, and first-time buyers are experiencing rare leverage with elevated inventory and substantial rebates.

For self-employed borrowers, rates of 5.9%-6.4% require proactive planning, strong documentation, and exploration of alternative lenders. For investors, the new rules demand independent property qualification and more conservative leverage strategies. For first-time buyers, this is a window of opportunity to negotiate favorable terms before potential stress test changes drive prices higher later in 2026.

The common thread? Personalized strategy matters more than ever. Generic advice won’t cut it when investor rules, rate environments, and qualification criteria vary so dramatically by borrower type.

Take Action Today

Don’t navigate the Toronto Mortgage Shake-Up April 2026 alone. Whether you’re a real estate investor adapting to new rules, a first-time buyer capitalizing on current opportunities, or a self-employed borrower seeking competitive rates, speaking with an experienced mortgage broker is your best first step.

The Everything Mortgages team specializes in Toronto’s unique market dynamics and has helped thousands of borrowers secure optimal financing under changing conditions. We have access to multiple lenders, understand the nuances of the new 2026 rules, and can create a customized strategy for your specific situation.

Ready to explore your options? Contact Everything Mortgages today for a personalized consultation. We’ll review your situation, compare lender options, and help you secure the best possible mortgage terms in April 2026’s evolving landscape.

📞 Get started now: Contact Everything Mortgages for expert guidance tailored to your unique needs.