Last updated: March 25, 2026

Quick Answer: A first-time home buyer in Canada can access several federal and provincial programs that reduce the upfront cost of buying a home, including the First Home Savings Account (FHSA), the Home Buyers' Plan (RRSP withdrawal up to $60,000), a federal tax credit worth up to $1,500, and a brand-new GST/HST rebate of up to $50,000 on newly built homes. The buying process typically takes 3 to 6 months from saving to closing, and qualifying generally requires a minimum 5% down payment, a credit score above 620, and passing the mortgage stress test.

Key Takeaways

- Who qualifies: You must not have owned a home that you lived in at any point in the previous four calendar years to be considered a first-time buyer under most federal programs.

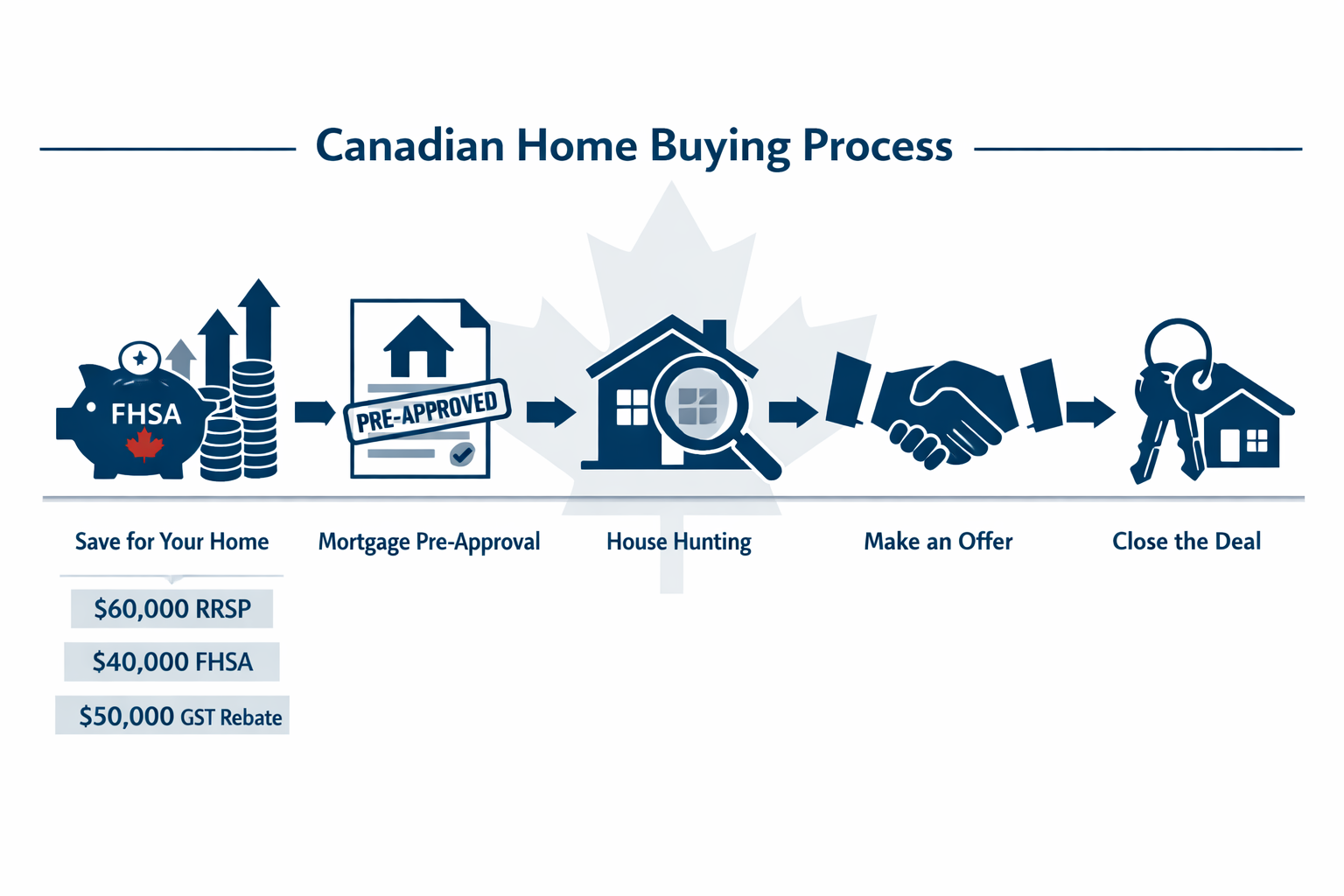

- FHSA: Contribute up to $8,000 per year (lifetime max $40,000) in a tax-free account specifically for your first home purchase.

- Home Buyers' Plan: Withdraw up to $60,000 tax-free from your RRSP (as of April 2024), repayable over 15 years starting two years after withdrawal. [1]

- New GST/HST rebate: As of March 17, 2026, eligible first-time buyers of newly built homes can receive a rebate of up to $50,000 through the CRA. [5]

- Federal tax credit: Claim up to $10,000 on your tax return in the year you buy, worth up to $1,500 in actual tax savings. [3]

- Provincial programs: Ontario, BC, and Quebec each offer land transfer tax rebates ranging from $5,000 to $15,000 depending on the province and purchase price. [1]

- Stress test: All insured mortgages must qualify at the higher of 5.25% or your contract rate plus 2%, regardless of your actual mortgage rate.

- Minimum down payment: 5% on homes up to $500,000; 10% on the portion between $500,000 and $999,999; 20% on homes $1 million and over.

What Does "First-Time Home Buyer" Mean in Canada?

In Canada, a first-time home buyer is generally someone who has not owned a home they lived in as their principal residence during the four calendar years before the purchase date. This definition applies to most federal programs, though some provincial programs use slightly different criteria.

A few important nuances:

- Couples: If one partner has owned a home before but the other hasn't, only the first-time buyer partner qualifies for certain credits. For the Home Buyers' Plan, each person must independently meet the definition.

- Previously owned but not occupied: If you owned a rental property but never lived in it as your primary home, you may still qualify as a first-time buyer under federal rules.

- Separated or divorced individuals: Someone who has been separated or divorced may regain first-time buyer status even if they previously owned a home with a spouse.

💡 Edge case: The four-year lookback window means someone who sold their last home in early 2022 could qualify again as a first-time buyer in 2026.

What Programs Are Available for First-Time Home Buyers in Canada?

Canada offers multiple stacked programs for first-time buyers, and using them together can save tens of thousands of dollars. Here is a breakdown of the major options available in 2026. [1][4]

Federal Programs

| Program | Benefit | Key Limit |

|---|---|---|

| First Home Savings Account (FHSA) | Tax-deductible contributions; tax-free withdrawals | $8,000/year, $40,000 lifetime |

| Home Buyers' Plan (RRSP) | Withdraw up to $60,000 tax-free | Repay over 15 years |

| First-Time Home Buyers' Tax Credit | Up to $1,500 tax savings | $10,000 claim on tax return |

| New GST/HST Rebate (2026) | Up to $50,000 rebate on new builds | Newly constructed/substantially renovated homes |

| Standard GST/HST New Housing Rebate | Up to $6,300 on homes under $350,000 | Phases out between $350K–$450K |

Provincial Programs (Selected)

| Province | Program | Maximum Benefit |

|---|---|---|

| Ontario | Land Transfer Tax Rebate | Up to $8,475 |

| British Columbia | Land Transfer Tax Rebate | Up to $8,000 (homes up to $525,000) |

| Quebec | Land Transfer Tax Rebate | $5,000–$15,000 (homes $225K–$630K) |

| Montreal | Home Purchase Assistance Program | Varies; principal residence required for 3+ years |

Common mistake: Many buyers claim only one or two programs when they could stack several. For example, using the FHSA, the Home Buyers' Plan, and the federal tax credit together is fully permitted and can significantly reduce both your tax bill and your upfront costs. [6]

How Does the First Home Savings Account (FHSA) Work?

The FHSA is the most powerful savings tool available to first-time home buyers in Canada right now. It combines the best features of an RRSP (contributions are tax-deductible) and a TFSA (qualifying withdrawals are tax-free), making it uniquely effective for home savings. [1]

Key rules:

- Contribute up to $8,000 per year, with a lifetime maximum of $40,000.

- Unused contribution room carries forward by one year only (so a maximum of $16,000 can be contributed in a single year if the prior year's room was unused).

- The account must be open for at least one calendar year before you make a qualifying withdrawal.

- Funds not used for a home purchase can be transferred to an RRSP or RRIF without tax consequences.

For a deeper look at how this account works and how to open one, see this introduction to the First Home Savings Account and this guide on how the tax-free FHSA can help you buy a house.

Choose the FHSA if: You expect to buy within the next 1 to 15 years, you have earned income, and you want both a tax deduction now and tax-free growth later.

How Does the Home Buyers' Plan Work in 2026?

The Home Buyers' Plan (HBP) lets first-time buyers withdraw funds from their RRSP to use as a down payment, without triggering immediate income tax. Since April 16, 2024, the withdrawal limit increased from $35,000 to $60,000 per person — meaning a couple buying together could access up to $120,000 combined from their RRSPs. [1]

Repayment rules:

- Repayment begins two years after the year of withdrawal.

- The full amount must be repaid over 15 years.

- If you miss a repayment in a given year, that missed amount is added to your taxable income for that year.

For more detail on how the HBP interacts with your overall retirement savings strategy, see RRSPs and the Home Buyers' Plan: What You Need to Know.

Edge case: If you contribute to your RRSP specifically to use the HBP, the funds must sit in the account for at least 90 days before withdrawal, or the contribution won't be deductible.

What Is the New First-Time Home Buyers' GST/HST Rebate?

On March 17, 2026, the Canada Revenue Agency announced a new First-Time Home Buyers' GST/HST Rebate, and applications are now open. This is one of the most significant new benefits for first-time buyers in years. [5]

What it covers:

- Eligible first-time buyers purchasing a newly constructed or substantially renovated home can receive a rebate of up to $50,000.

- This is separate from the existing GST/HST New Housing Rebate, which offers up to $6,300 on homes priced under $350,000, with a gradual phase-out for homes between $350,000 and $450,000, and no federal rebate above $450,000. [4]

How to apply: Applications are submitted through the CRA. Buyers should confirm eligibility based on the home type, purchase price, and their first-time buyer status before applying.

🏠 Pull quote: "The new GST/HST rebate of up to $50,000 on newly built homes marks a major shift in federal housing affordability support for first-time buyers in Canada." — CRA, March 2026 [5]

What Are the Steps to Buying Your First Home in Canada?

Buying a first home in Canada follows a clear sequence. Skipping steps — especially getting pre-approved before making offers — is one of the most common and costly mistakes first-time buyers make. For a full breakdown of common pitfalls, see first-time home buyer mistakes to avoid.

Step-by-step process:

- Check your credit score. Aim for 620 or higher for insured mortgages; 680+ for better rates. Learn how to improve your credit score if needed.

- Open an FHSA and/or contribute to your RRSP. Start at least one year before you plan to buy to maximize FHSA withdrawal eligibility.

- Calculate your budget. Factor in down payment, closing costs (typically 1.5–4% of purchase price), land transfer taxes, and legal fees.

- Get mortgage pre-approval. This confirms your borrowing limit and locks in a rate for 90–120 days. See the ins and outs of mortgage pre-approval in Ontario.

- Pass the mortgage stress test. You must qualify at the higher of 5.25% or your contract rate plus 2%. Understand how the stress test works.

- Search for a property. Work with a real estate agent who knows your target market.

- Make an offer and negotiate. Include conditions for financing and home inspection.

- Complete due diligence. Home inspection, title search, and review of legal fees.

- Close the deal. Sign documents, pay closing costs, and receive your keys.

Timeframe: Most first-time buyers in Canada take 3 to 6 months from pre-approval to closing, though the saving phase before that can take 2 to 5 years depending on income and target price.

How Much Down Payment Do First-Time Buyers in Canada Need?

The minimum down payment in Canada depends on the purchase price of the home. Mortgage default insurance (from CMHC, Sagen, or Canada Guaranty) is required whenever the down payment is less than 20%.

| Purchase Price | Minimum Down Payment |

|---|---|

| Up to $500,000 | 5% |

| $500,001 to $999,999 | 5% on first $500K + 10% on remainder |

| $1,000,000 and above | 20% (no insured mortgage available) |

Closing costs to budget for separately:

- Land transfer tax (federal and/or provincial)

- Legal fees (typically $1,500–$3,000 in Ontario; see legal fees for Toronto homebuyers)

- Home inspection ($400–$600)

- Title insurance ($200–$400)

- Moving costs

Decision rule: If you can put 20% down, you avoid CMHC insurance premiums (which range from 0.60% to 4.00% of the mortgage amount). But waiting to save 20% in a rising market can cost more than the insurance itself — run the numbers for your specific situation.

What Credit Score and Income Do You Need?

Most lenders require a minimum credit score of 620 for an insured mortgage in Canada, though a score of 680 or higher typically qualifies for better rates and more lender options. [8]

Income requirements:

- Lenders use your gross debt service (GDS) ratio (housing costs as a percentage of gross income, max 39%) and total debt service (TDS) ratio (all debt payments, max 44%).

- Most first-time buyer incentive programs also cap household income at $120,000, or $150,000 in Toronto, Vancouver, or Victoria census metropolitan areas. [4]

- Self-employed buyers face additional documentation requirements. See opportunities for first-time homebuyers among self-employed Canadians for more detail.

Common mistake: Applying for new credit cards or car loans in the months before a mortgage application. New credit inquiries and increased debt can lower your score and raise your TDS ratio right when lenders are reviewing your file.

What Provincial and Municipal Programs Should First-Time Buyers Know About?

Beyond federal programs, several provinces and municipalities offer additional support for first-time home buyers in Canada that can meaningfully reduce closing costs. [1][3]

Ontario:

- Land transfer tax rebate of up to $8,475 (no maximum home price restriction).

- Toronto buyers also pay a municipal land transfer tax but receive a matching rebate of up to $4,475.

British Columbia:

- Land transfer tax (Property Transfer Tax) rebate of up to $8,000 for homes up to $525,000. [1]

- The BC Home Owner Mortgage and Equity Partnership offers low-cost loans of up to 5% of the purchase price (maximum $37,500 for resale homes, $40,000 for new builds). [4]

Quebec:

- Land transfer tax rebate ranging from $5,000 to $15,000 for homes priced between $225,000 and $630,000. [1]

- Montreal's Home Purchase Assistance Program is available to buyers who haven't owned property in the previous five years and commit to using the property as their principal residence for at least three years. [3]

Other municipalities: Some cities offer down payment assistance programs (DPAPs) for first-time buyers. Availability and amounts vary significantly by location, so check with your local municipality directly. [1]

Is 2026 a Good Time to Buy a First Home in Canada?

For many first-time buyers, 2026 presents a more balanced market than the peak years of 2021 and 2022. Interest rates have moderated from their 2023 highs, and inventory has improved in many markets, giving buyers more negotiating room.

Key factors working in buyers' favor in 2026:

- More inventory in major urban centers, including the GTA and Metro Vancouver.

- Stabilizing prices in many markets compared to the sharp increases seen earlier in the decade.

- New government programs like the expanded GST/HST rebate launched in March 2026. [5]

- 30-year amortization now available for first-time buyers on new construction, reducing monthly payments. See 30-year amortization for first-time buyers.

That said, affordability remains a challenge in Toronto and Vancouver specifically. If you're in the GTA, this analysis of whether 2026 is the right time to enter Toronto's housing market offers a detailed breakdown.

Choose to buy now if: You have a stable income, a solid down payment, and plan to stay in the home for at least 5 years. Trying to time the market perfectly rarely works better than buying when you're financially ready.

Frequently Asked Questions

Q: Can I use both the FHSA and the Home Buyers' Plan together?

Yes. You can withdraw from both your FHSA and your RRSP (via the HBP) for the same home purchase. There is no rule against stacking these two programs. [1]

Q: What happens if I don't repay my Home Buyers' Plan withdrawal?

Any amount you don't repay in a given year is added to your taxable income for that year. Missing repayments doesn't cancel the plan, but it increases your annual tax bill.

Q: Is the First-Time Home Buyer Incentive (FTHBI) still available?

No. The CMHC-administered shared-equity mortgage program was discontinued in March 2024. It is no longer accepting new applications. [1]

Q: Do I qualify as a first-time buyer if my spouse has owned a home before?

It depends on the program. For the federal tax credit and HBP, each person is assessed individually. If your spouse owned a home they lived in during the past four years, they don't qualify — but you may still qualify on your own portion.

Q: What is the mortgage stress test and can I avoid it?

The stress test requires you to qualify at the higher of 5.25% or your actual rate plus 2%. All federally regulated lenders must apply it to insured mortgages. You cannot avoid it by choosing a different lender if that lender is federally regulated.

Q: How long does it take to get mortgage pre-approval in Canada?

Most lenders can provide a pre-approval within 1 to 3 business days if you have your documents ready (T4s, NOAs, pay stubs, bank statements, and ID).

Q: Can I buy a home in Canada if I'm self-employed?

Yes, though lenders require additional documentation such as two years of T1 generals and business financials. Some lenders specialize in self-employed borrowers.

Q: What closing costs should I budget for beyond the down payment?

Plan for 1.5% to 4% of the purchase price in closing costs, covering land transfer taxes, legal fees, title insurance, home inspection, and adjustments.

Q: Is CMHC mortgage insurance mandatory if I put less than 20% down?

Yes. Any home purchase with less than 20% down requires mortgage default insurance from CMHC, Sagen, or Canada Guaranty. The premium ranges from 0.60% to 4.00% of the mortgage amount and is typically added to the mortgage balance.

Q: Can a non-permanent resident buy a home in Canada as a first-time buyer?

Permanent residents and Canadian citizens qualify for all standard first-time buyer programs. Temporary residents face restrictions under the foreign buyer ban (in effect since 2023), with some exceptions. Confirm your status with a mortgage professional.

Conclusion: Your Next Steps as a First-Time Home Buyer in Canada

Buying your first home in Canada is one of the largest financial decisions you'll make — but the combination of federal programs, provincial rebates, and new 2026 incentives means there's more support available right now than at almost any point in recent history.

Actionable next steps:

- Open an FHSA today if you haven't already. Even if you're not buying for a year or two, the clock on qualifying withdrawals starts from the day the account is opened.

- Check your RRSP balance and understand how the Home Buyers' Plan could supplement your down payment.

- Review the new GST/HST rebate if you're considering a newly built home — the up to $50,000 rebate launched March 17, 2026 could significantly change your purchase math.

- Get a mortgage pre-approval before you start seriously searching. It protects your rate and clarifies your real budget.

- Research provincial programs specific to your location — Ontario, BC, and Quebec each have meaningful rebates that stack on top of federal benefits.

- Work with a licensed mortgage broker who can help you identify every program you qualify for and find the best rate for your situation.

For a complete savings roadmap, see how to save and buy your first home: a complete guide for first-time buyers.

The path to homeownership in Canada is clearer when you know what tools are available. Start with the savings accounts, understand the programs, and build your team early.

References

[1] First Time Home Buyer Canada – https://wowa.ca/calculators/first-time-home-buyer-canada

[2] Government Canada Homebuyer Programs – https://www.lowestrates.ca/blog/homes/government-canada-homebuyer-programs

[3] First Time Homebuyer Incentives In Canada – https://blog.remax.ca/first-time-homebuyer-incentives-in-canada/

[4] First Time Buyer Incentives Canada 2026 – https://ratefair.ca/first-time-buyer-incentives-canada-2026/

[5] First Time Buyers Can Save More On New Homes: The First-Time Home Buyers' GST/HST Rebate Is Available Now – https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2026/first-time-buyers-can-save-more-on-new-homes-the-first-time-home-buyers-gst-hst-rebate-is-available-now.html

[6] 5 First Time Home Buyer Incentives – https://www.sunlitemortgage.ca/5-first-time-home-buyer-incentives/

[7] Government Of Canada Programs To Support Homebuyers – https://www.cmhc-schl.gc.ca/consumers/home-buying/government-of-canada-programs-to-support-homebuyers

[8] First Time Home Buyer Grants & Assistance – https://www.nerdwallet.com/ca/p/article/mortgages/first-time-home-buyer-grants-assistance

Tags: first-time home buyer canada, FHSA, Home Buyers Plan, RRSP withdrawal, GST HST rebate, mortgage stress test, down payment canada, land transfer tax rebate, CMHC mortgage insurance, first-time buyer programs, home buying canada, canadian housing market 2026