25 Mar

Last updated: March 25, 2026

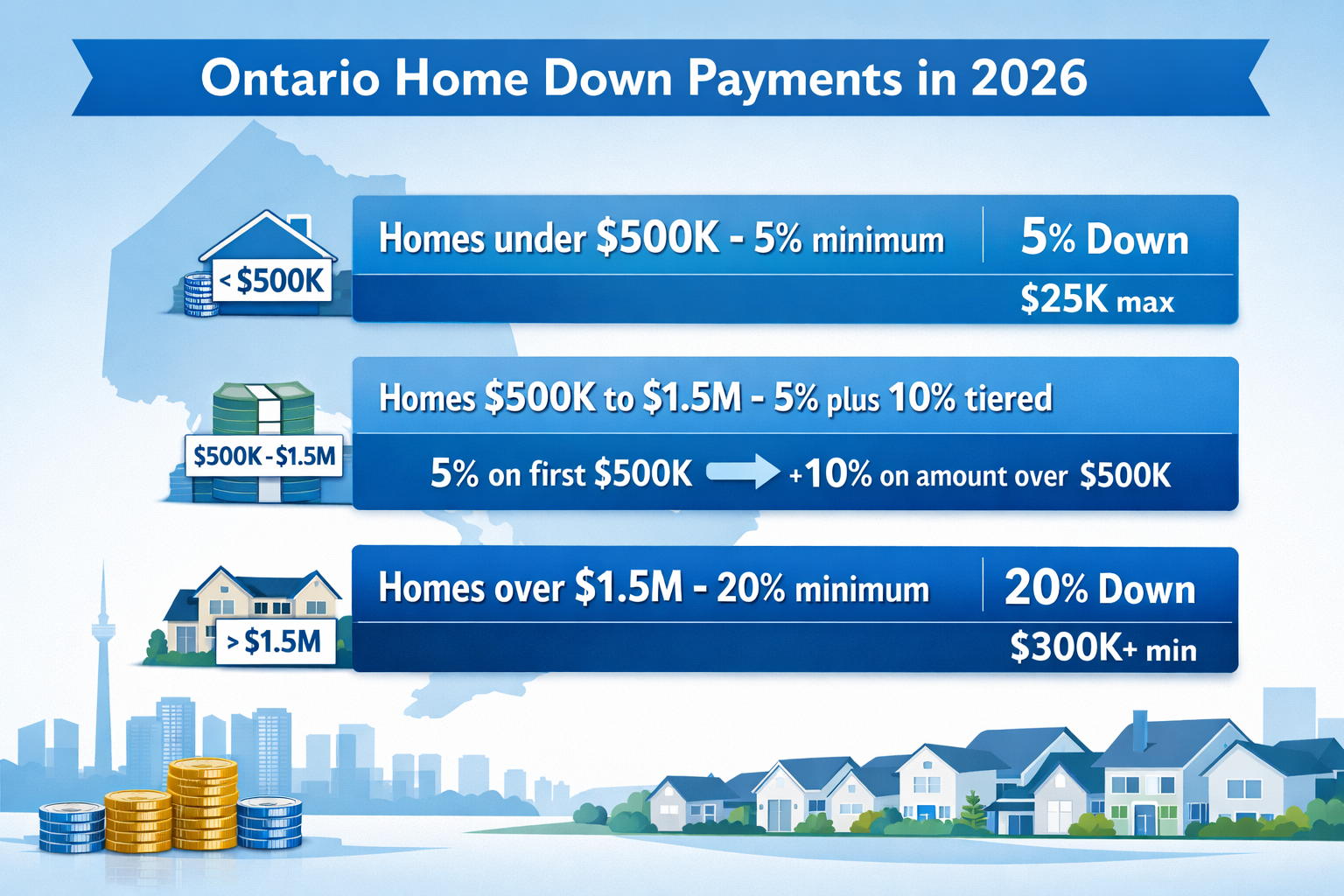

Quick Answer: In Ontario, the minimum down payment for first time home buyers depends on the purchase price. Homes under $500,000 require at least 5% down. Homes priced between $500,000 and $1.5 million use a tiered formula. Homes above $1.5 million require 20% down with no mortgage insurance available. Several provincial and federal programs can help buyers reach their target down payment faster.

Key Takeaways

- 5% minimum down payment applies to Ontario homes priced at $500,000 or less [2]

- Tiered formula applies between $500,000 and $1.5 million: 5% on the first $500,000, then 10% on the remainder [2]

- 20% minimum is required for any home over $1.5 million, with no mortgage default insurance option [2]

- Mortgage default insurance (CMHC insurance) is mandatory when putting down less than 20%, and the premium is added to the mortgage balance [2]

- The Home Buyers’ Plan lets eligible first-time buyers withdraw up to $35,000 (or up to $60,000 for couples) from their RRSP tax-free for a down payment [6]

- Ontario offers a land transfer tax refund of up to $4,000 for qualifying first-time buyers [8]

- The federal First-Time Home Buyer Incentive program is no longer accepting applications as of March 2026 [9]

- New rules introduced in December 2024 expanded access for first-time buyers, including extended amortization periods [1]

- A standard deposit of roughly 5% is typically paid when an offer is accepted, and this amount counts toward the final down payment at closing [1]

- Avoiding common mistakes early in the process can save thousands — see our guide on first-time home buyer mistakes

What Are the Minimum Down Payment Requirements for First Time Home Buyers in Ontario?

The minimum down payment in Ontario follows a tiered structure based on the home’s purchase price. These rules apply to all buyers, but first-time buyers have access to additional programs that can help them meet these thresholds.

Here is a clear breakdown of the current requirements as of 2026:

| Purchase Price | Minimum Down Payment |

|---|---|

| $500,000 or less | 5% of purchase price |

| $500,001 to $1,500,000 | 5% on first $500K + 10% on remainder |

| Over $1,500,000 | 20% of full purchase price |

Example: For a $750,000 home, the minimum down payment is calculated as:

- 5% of $500,000 = $25,000

- 10% of $250,000 = $25,000

- Total minimum down payment: $50,000

December 2024 rule change: Before December 2024, the tiered formula only applied to homes up to $999,999. The threshold was raised to $1.5 million, meaning buyers can now purchase homes up to $1.5 million with less than 20% down, provided they meet other lending criteria [1].

Common mistake: Many buyers assume the 5% rule applies to any home price. For a $900,000 property, the actual minimum is $65,000, not $45,000. Running the tiered calculation before starting the home search prevents budget surprises.

Why Does Mortgage Default Insurance Apply to First Time Home Buyers in Ontario?

Any buyer, including first-time buyers, who puts down less than 20% of the purchase price is required by law to carry mortgage default insurance. This protects the lender, not the buyer, if the mortgage goes into default.

Key facts about mortgage default insurance:

- Premiums are calculated as a percentage of the mortgage amount (not the purchase price)

- The premium is added to the total mortgage balance, not paid upfront in most cases

- Insurance is provided through CMHC, Sagen, or Canada Guaranty

- Insured mortgages are limited to homes priced under $1.5 million [2]

Premium rate table (approximate, based on loan-to-value ratio):

| Down Payment | Loan-to-Value | Insurance Premium |

|---|---|---|

| 5% | 95% | 4.00% of mortgage |

| 10% | 90% | 3.10% of mortgage |

| 15% | 85% | 2.80% of mortgage |

| 20%+ | 80% or less | No insurance required |

Choose 20% down if: The goal is to eliminate the insurance premium entirely and reduce the total cost of the mortgage over time. However, waiting to save 20% in Ontario’s market means a longer timeline, so many first-time buyers accept the insurance cost to enter the market sooner.

Understanding how the stress test works alongside these requirements is also important. Read more in our guide to the mortgage stress test for home buyers in Canada.

What Programs Help First Time Home Buyers in Ontario With Their Down Payment?

Several programs directly reduce the amount first-time buyers need to save on their own. The most useful ones in 2026 are the Home Buyers’ Plan and Ontario’s land transfer tax refund.

1. Home Buyers’ Plan (HBP)

The Home Buyers’ Plan allows eligible first-time buyers to withdraw funds from their RRSP tax-free to use toward a down payment [6].

- Individual limit: Up to $35,000 per person

- Couple limit: Up to $60,000 combined (if both qualify as first-time buyers)

- The withdrawn amount must be repaid to the RRSP over 15 years

- Funds must have been in the RRSP for at least 90 days before withdrawal

Edge case: If repayments are missed, the outstanding amount is added to taxable income for that year. Buyers who plan to use the HBP should build repayment into their long-term budget from the start.

2. First Home Savings Account (FHSA)

The FHSA is a registered account that combines features of an RRSP and a TFSA specifically for first-time buyers.

- Annual contribution limit: $8,000

- Lifetime contribution limit: $40,000

- Contributions are tax-deductible

- Withdrawals for a qualifying home purchase are tax-free

- Unused room carries forward (up to $8,000 per year)

The FHSA and HBP can be used together, which means a couple could potentially combine FHSA savings with HBP withdrawals for a significant combined down payment contribution.

3. Ontario Land Transfer Tax Refund

Ontario first-time buyers can receive a refund of the provincial land transfer tax up to $4,000 [8]. Toronto buyers may also qualify for a separate municipal land transfer tax refund of up to $4,475.

- The refund applies automatically when the property is registered

- The home must be a new principal residence

- Buyers must never have owned a home anywhere in the world before

4. Federal First-Time Home Buyer Incentive (Closed)

This shared-equity program offered by the federal government is no longer accepting new applications as of March 2026 [9]. Buyers who applied before the deadline may still be in the process, but this option is not available for new applicants.

For more context on how this program worked and what replaced it, see our earlier coverage of the First-Time Home Buyers Incentive program.

How Much Should First Time Home Buyers in Ontario Actually Save for a Down Payment?

The minimum down payment is the legal floor, but it is rarely the ideal target. First-time buyers in Ontario should plan for additional costs beyond the down payment itself.

Costs to budget beyond the down payment:

- Closing costs: Typically 1.5% to 4% of the purchase price (legal fees, title insurance, home inspection, adjustments)

- Land transfer tax: Provincial and potentially municipal, partially offset by the first-time buyer refund

- Home inspection: $400 to $600 on average

- Moving costs: Variable

- CMHC insurance premium: Added to the mortgage but worth factoring into total debt

Pull quote: “The minimum down payment gets you in the door, but buyers who budget for closing costs avoid the stress of scrambling for cash at the last minute.”

Practical savings targets by price range (Ontario, 2026):

| Home Price | Minimum Down | Estimated Closing Costs | Suggested Total Savings |

|---|---|---|---|

| $500,000 | $25,000 | $7,500–$20,000 | $35,000–$45,000 |

| $750,000 | $50,000 | $11,000–$30,000 | $65,000–$80,000 |

| $1,000,000 | $75,000 | $15,000–$40,000 | $95,000–$115,000 |

| $1,500,000 | $125,000 | $22,000–$60,000 | $150,000–$185,000 |

For practical strategies to build savings faster, the saving tips to become mortgage free resource covers approaches that work for Ontario buyers at different income levels.

What Is a Deposit and How Does It Relate to the Down Payment?

A deposit and a down payment are not the same thing, though buyers often confuse them. The deposit is paid when an offer is accepted, while the down payment is the full amount confirmed at closing.

How deposits work in Ontario:

- A deposit is typically around 5% of the purchase price [1]

- It is paid to the seller’s real estate brokerage and held in trust

- The deposit is applied toward the total down payment at closing

- If the deal falls through due to a condition not being met, the deposit is usually returned

- If the buyer walks away without a valid condition, the deposit may be forfeited

Example: On a $700,000 home, a buyer might pay a $35,000 deposit when the offer is accepted. At closing, this $35,000 is applied to the total down payment. If the buyer’s minimum down payment is $57,500, they would need to bring an additional $22,500 at closing (plus closing costs).

Slightly higher deposits above 5% are common in competitive markets and can make an offer more attractive to sellers [1].

How Do Extended Amortization Periods Affect First Time Home Buyers’ Down Payments?

New rules introduced in late 2024 allow first-time buyers to access extended amortization periods, which changes the monthly payment calculation but does not change the minimum down payment requirement.

What changed:

- First-time buyers purchasing a new or existing home can now access 30-year amortization periods [10]

- Previously, insured mortgages (less than 20% down) were capped at 25 years

- A longer amortization lowers monthly payments, making it easier to qualify under the stress test

- The trade-off is paying more interest over the life of the mortgage

Choose a 30-year amortization if: Monthly cash flow is tight and the priority is qualifying now rather than paying off the mortgage faster. Choose a 25-year amortization if the goal is to minimize total interest paid.

For buyers deciding between property types, the choice of condo versus house also affects how much down payment is needed and what amortization makes sense. The guide on home purchase in Ontario: condo versus house breaks down the financial differences clearly.

What Are the Biggest Down Payment Mistakes First Time Buyers in Ontario Make?

Most down payment mistakes come down to timing, source of funds, or underestimating total costs.

Most common mistakes:

Using gifted funds without documentation: Lenders require a signed gift letter confirming the money does not need to be repaid. Without it, the gift may be treated as a loan, which affects borrowing capacity.

Moving money between accounts too close to closing: Lenders verify the source of down payment funds. Large, unexplained transfers within 90 days of application raise flags.

Forgetting closing costs: Many buyers save exactly the minimum down payment and then discover they need an additional $15,000 to $30,000 for closing. This can delay or derail a purchase.

Withdrawing RRSP funds without checking the 90-day rule: Funds must sit in the RRSP for at least 90 days before withdrawal under the Home Buyers’ Plan. Timing matters.

Assuming the First-Time Home Buyer Incentive is still available: The federal shared-equity program closed to new applicants in March 2026 [9]. Buyers who budget for this program will need to find alternative sources.

Skipping mortgage pre-approval: Without pre-approval, buyers don’t know their actual borrowing limit, which makes it impossible to set a realistic down payment target.

For a more complete list of pitfalls, the guide on first-time home buyer mistakes covers scenarios that catch many Ontario buyers off guard.

How Does Having a Co-Signer Affect the Down Payment for First Time Buyers?

A co-signer does not directly reduce the required down payment, but they can help a buyer qualify for a larger mortgage, which changes the math on how much needs to be saved.

How co-signing works:

- The co-signer’s income and credit are included in the mortgage application

- This can increase the maximum mortgage a lender will approve

- The down payment percentage requirements remain the same regardless of who co-signs

- The co-signer is equally responsible for the mortgage if the primary buyer defaults

When co-signing makes sense: A first-time buyer with a stable income but limited credit history may benefit from a co-signer to qualify for a better rate or higher purchase price. The co-signer does not need to live in the home.

For a full breakdown of the responsibilities and risks involved, see the guide on co-signing on a mortgage in Canada.

Frequently Asked Questions

Q: Can I use a personal loan or line of credit for my down payment in Ontario? A: Most lenders do not accept borrowed funds as a down payment for insured mortgages (less than 20% down). For conventional mortgages (20% or more), some lenders allow it, but the debt payments are factored into your debt service ratios, which reduces how much mortgage you qualify for.

Q: What counts as an acceptable source of down payment funds? A: Lenders accept savings, RRSP withdrawals (via the Home Buyers’ Plan), FHSA withdrawals, gifted funds from immediate family (with a signed gift letter), and proceeds from the sale of another property.

Q: Is the 5% minimum down payment the same across all of Ontario? A: Yes. The minimum down payment rules are federal, so they apply equally whether the home is in Toronto, Ottawa, Hamilton, or a smaller Ontario city. What changes is the purchase price, which affects which tier applies.

Q: How long does it take to save a down payment for an Ontario home? A: This varies significantly by income, expenses, and target price. Using the FHSA (up to $8,000 per year, tax-deductible) alongside regular savings can accelerate the timeline. A couple maximizing FHSA contributions for five years could accumulate $80,000 in dedicated down payment savings before accounting for investment growth.

Q: Can the land transfer tax refund be used as part of the down payment? A: No. The Ontario land transfer tax refund of up to $4,000 is applied at closing and reduces the amount of tax owed. It does not provide cash before the purchase that can be used as a down payment.

Q: What happens if my down payment comes from multiple sources? A: Lenders require documentation for each source. Mixing RRSP withdrawals, FHSA funds, and gifted money is acceptable, but each source needs its own paper trail. Organize statements and letters well before the application.

Q: Does the first-time buyer definition reset if I’ve owned a home before? A: Under federal rules, a buyer qualifies as a first-time buyer if they have not owned a principal residence at any time during the preceding four calendar years. Some provincial programs have stricter definitions requiring no prior ownership at all.

Q: Is there a maximum purchase price for first-time buyer programs in Ontario? A: The Home Buyers’ Plan and FHSA have no purchase price cap. The Ontario land transfer tax refund applies to any qualifying purchase. The insured mortgage limit (requiring CMHC insurance) is $1.5 million, meaning homes above that price require 20% down and cannot be insured.

Q: What is the stress test rate for first-time buyers in 2026? A: The mortgage stress test requires buyers to qualify at either the contract rate plus 2%, or the Bank of Canada’s qualifying rate (whichever is higher). This applies to all buyers, including first-time buyers, regardless of down payment size.

Q: Can I buy a home in Ontario with less than 5% down? A: No. Five percent is the federal minimum for any insured mortgage in Canada. There are no programs in Ontario that allow a lower down payment on a standard residential purchase.

Conclusion: Actionable Next Steps for First Time Home Buyers in Ontario

Understanding the first time home buyers Ontario down payment rules is the foundation of a successful purchase. The requirements are clear, but the path to meeting them involves more than just saving the minimum percentage.

Here are the most important next steps to take in 2026:

- Open an FHSA immediately if eligible. Every year without one is $8,000 in contribution room lost permanently.

- Check RRSP balances and confirm whether the 90-day rule is met before planning an HBP withdrawal.

- Calculate the tiered down payment for your target price range, not just the base 5%.

- Budget for closing costs separately from the down payment, targeting an additional 2% to 4% of the purchase price.

- Get pre-approved before making offers. Pre-approval confirms the actual borrowing limit and identifies any documentation gaps early.

- Document all savings sources from the start. Lenders will ask for 90 days of bank statements, so unexplained deposits should be addressed well before application.

- Consult a mortgage professional to model different down payment scenarios, amortization lengths, and program combinations specific to your situation.

The rules changed significantly in December 2024, and more updates may follow. Staying current on program eligibility and lending requirements ensures that first-time buyers in Ontario make decisions based on accurate information, not outdated assumptions.

References

[1] Watch (Ontario Home Buying Guide) – https://www.youtube.com/watch?v=Hgjl_knuV1w [2] First Time Home Buyer Programs – https://www.ratehub.ca/first-time-home-buyer-programs [4] First Time Home Buyer Programs Incentives For Toronto Home Buyers – https://www.elevatepartners.ca/resources/first-time-home-buyer-programs-incentives-for-toronto-home-buyers/ [6] First Time Homebuyer Incentives In Canada – https://blog.remax.ca/first-time-homebuyer-incentives-in-canada/ [7] Down Payment Assistance Programs – https://citadelmortgages.ca/down-payment-assistance-programs/ [8] First Time Home Buyer Canada – https://wowa.ca/calculators/first-time-home-buyer-canada [9] First Time Home Buyer Incentive – https://www.cmhc-schl.gc.ca/consumers/home-buying/first-time-home-buyer-incentive [10] 30 Year Mortgage For First Time Homebuyers And To All Buyers Of New Builds – https://cornerstone.inc/2025/09/30/30-year-mortgage-for-first-time-homebuyers-and-to-all-buyers-of-new-builds/

Tags: first time home buyers ontario, ontario down payment, minimum down payment ontario, CMHC mortgage insurance, Home Buyers Plan RRSP, FHSA first home savings account, ontario land transfer tax refund, mortgage stress test canada, first time buyer programs ontario, down payment assistance ontario, ontario real estate 2026, insured mortgage canada