25 Mar

Last updated: March 25, 2026

Quick Answer: The Government of Canada offers several programs to help first-time buyers enter the housing market, including the new First-Time Home Buyers’ GST/HST Rebate (up to $50,000), the First Home Savings Account (FHSA), the RRSP Home Buyers’ Plan, a First-Time Home Buyers’ Tax Credit, and access to 30-year amortization on insured mortgages. These programs can be combined, and the total savings can be substantial depending on the home price and province.

Key Takeaways

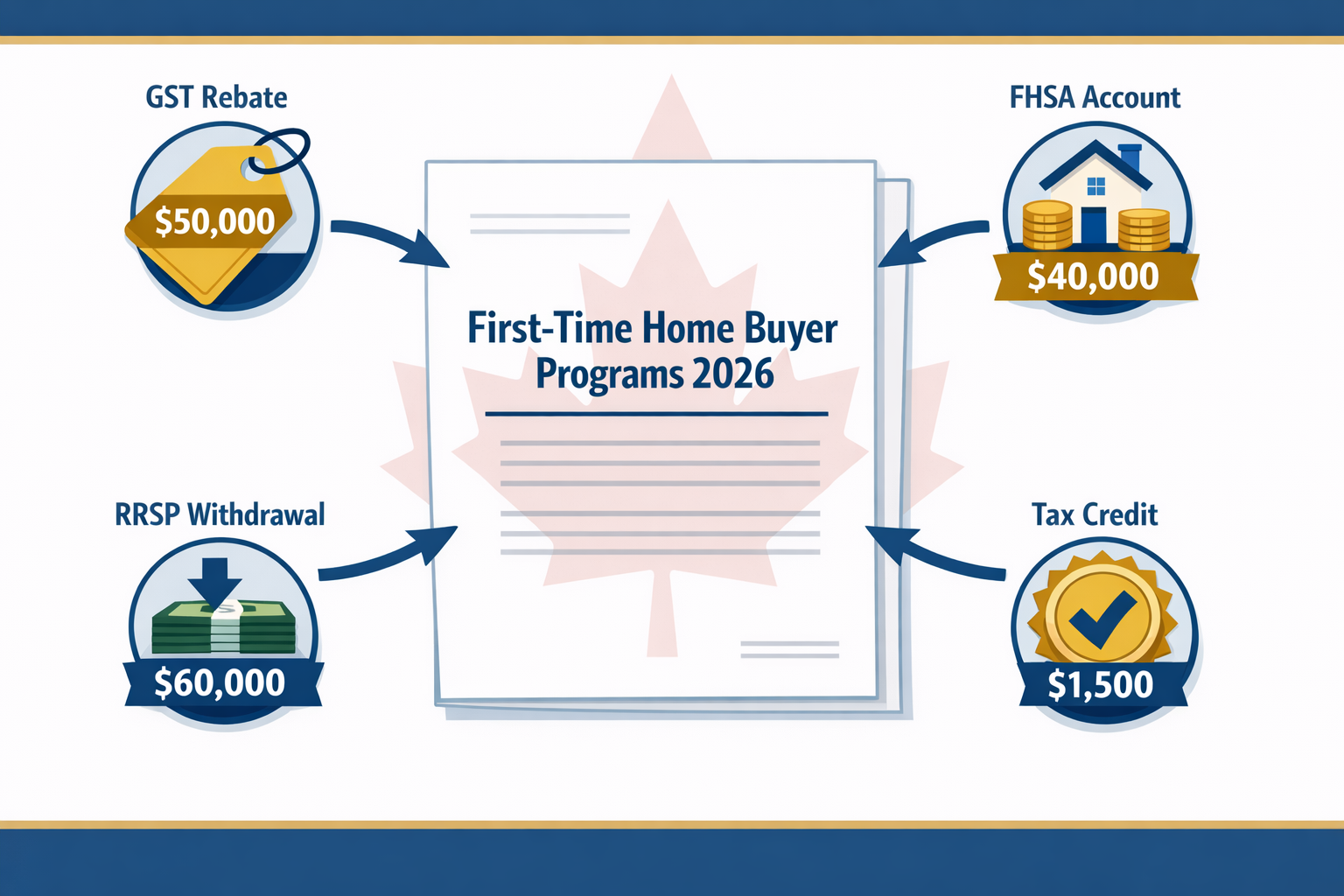

- 🏠 The First-Time Home Buyers’ GST/HST Rebate, launched March 17, 2026, provides up to $50,000 back on newly built or substantially renovated homes [2]

- 💰 The First Home Savings Account (FHSA) allows up to $40,000 per person ($80,000 per couple) in tax-deductible, tax-free savings for a home purchase [1]

- 📋 The RRSP Home Buyers’ Plan lets eligible buyers withdraw up to $60,000 tax-free from their RRSP for a down payment [1]

- 🧾 The First-Time Home Buyers’ Tax Credit provides up to $1,500 back on closing costs [1]

- 📅 As of December 2024, first-time buyers can access 30-year amortization on insured mortgages, reducing monthly payments [4]

- 🏙️ Provincial programs add more savings: Ontario offers up to $4,000 in land transfer tax rebates; Toronto adds another $4,475 [1]

- ✅ Most programs can be stacked together, meaning buyers can use the FHSA, RRSP plan, and tax credit at the same time

- ⚠️ The original First-Time Home Buyer Incentive (shared-equity mortgage) was officially ended by the federal government in 2024

- 🔑 Minimum down payment requirements remain: 5% for homes under $500,000, 10% for the portion between $500,000 and $1.5 million [1]

- 📝 Buyers have up to two years from taking ownership to apply for the GST/HST rebate [2]

What Is the First-Time Home Buyer Incentive Government of Canada, and What Replaced It?

The original First-Time Home Buyer Incentive was a shared-equity mortgage program where the Government of Canada contributed 5% or 10% toward a home purchase in exchange for a share of the property’s future value. That program was officially discontinued in 2024.

What replaced it is a broader, more generous set of programs. As of 2026, the first-time home buyer incentive landscape from the Government of Canada includes the new GST/HST rebate, expanded FHSA contribution room, an increased RRSP withdrawal limit, and extended mortgage amortization. Together, these tools offer more direct savings than the old shared-equity model.

Why it matters: The old program required repayment when the home was sold or after 25 years, based on the home’s market value at that time, which created uncertainty for buyers. The current programs are either outright grants, tax credits, or tax-free savings tools with no equity-sharing requirement.

What Is the New First-Time Home Buyers’ GST/HST Rebate?

The First-Time Home Buyers’ GST/HST Rebate is the most significant new federal benefit available in 2026. It refunds the full GST (or the federal portion of HST) on a newly constructed or substantially renovated home, up to a maximum of $50,000 [6].

The Canada Revenue Agency began accepting applications on March 17, 2026 [2].

How the rebate works

- Who qualifies: Canadian residents purchasing a newly built or substantially renovated home as their primary residence, who have not owned a home in the past four years

- Maximum benefit: $50,000, which equals approximately 5% GST on a $1 million home [6]

- Application deadline: Up to two years from taking ownership or completing construction [2]

- Builder credit option: Builders can apply the rebate directly at closing using Form GST190, so many buyers won’t need to file a separate application [2]

“First-time buyers purchasing a new home priced at $1 million could receive up to $50,000 back in GST — a meaningful reduction in one of the largest upfront costs of homeownership.” — Canada Revenue Agency, 2026 [2]

Common mistake to avoid

Many buyers assume the rebate only applies to purchases made after March 17, 2026. Check with the CRA or a tax professional for your specific closing date and eligibility window, since the two-year application period means some earlier purchases may still qualify.

For a deeper look at how the original incentive program launched and evolved, see this overview of the First-Time Home Buyers Incentive program launch.

How Does the First Home Savings Account (FHSA) Work?

The FHSA is a registered savings account that combines the best features of an RRSP and a TFSA specifically for first-time home buyers. Contributions are tax-deductible (like an RRSP), and withdrawals for a qualifying home purchase are tax-free (like a TFSA) [1].

FHSA at a glance

| Feature | Detail |

|---|---|

| Lifetime contribution limit | $40,000 per person |

| Annual contribution limit | $8,000 |

| Couple’s combined limit | $80,000 |

| Tax on contributions | Deductible from income |

| Tax on qualifying withdrawals | None |

| If unused | Transfer to RRSP/RRIF, no repayment required |

| Eligible account holders | Canadian residents, first-time buyers, age 18+ |

Choose the FHSA if…

- You have time to save before purchasing (the account grows tax-free)

- You want to reduce your taxable income now while saving for a home

- You’re planning to buy with a partner (both can open separate accounts, doubling the benefit)

Edge case: If you open an FHSA but don’t end up buying a home, the funds can be transferred to your RRSP without affecting your RRSP contribution room. There’s no penalty for changing plans.

What Is the RRSP Home Buyers’ Plan and Who Qualifies?

The RRSP Home Buyers’ Plan (HBP) allows first-time buyers to withdraw up to $60,000 tax-free from their RRSP to use toward a down payment [1]. The funds must be repaid over 15 years, starting two years after the year of withdrawal.

Eligibility requirements

- Must not have owned a home (or lived in a spouse/partner’s home) in the last four years [1]

- Must plan to use the home as a primary residence

- RRSP funds must have been in the account for at least 90 days before withdrawal [1]

- Must be a Canadian resident at the time of withdrawal

Combining HBP with the FHSA

A couple can combine both tools: each partner withdraws $60,000 from their RRSP and contributes up to $40,000 from their FHSA, potentially putting together a $200,000 down payment from registered accounts alone. This stacking strategy is one of the most powerful options available to first-time buyers in 2026.

Repayment note: Unlike FHSA withdrawals, RRSP withdrawals under the HBP must be repaid. If you miss a repayment in a given year, that amount is added to your taxable income for that year. Set up automatic annual repayments to avoid this.

What Other Federal Programs Help First-Time Home Buyers?

Beyond the GST rebate, FHSA, and RRSP plan, the Government of Canada offers two additional programs worth knowing [9].

First-Time Home Buyers’ Tax Credit (HBTC)

- A non-refundable tax credit of up to $1,500 [1]

- Calculated as 15% of $10,000 on eligible closing costs (legal fees, land transfer taxes, home inspections)

- Can be split between partners but the combined claim cannot exceed $10,000

- Applied when filing your income tax return for the year of purchase

30-Year Amortization on Insured Mortgages

As of December 2024, first-time buyers with less than 20% down payment can choose a 30-year amortization period instead of the standard 25-year maximum [4]. This lowers monthly mortgage payments, making homeownership more accessible in high-cost markets.

Choose a 30-year amortization if: monthly cash flow is tight and you need lower payments now, even if you pay more interest over the life of the mortgage.

Stick with 25 years if: you can comfortably afford the higher payments and want to build equity faster and pay less interest overall.

Understanding the mortgage stress test for home buyers in Canada is also essential before choosing your amortization period, since qualification is based on a qualifying rate higher than your contract rate.

What Provincial Programs Are Available for First-Time Buyers?

Provincial programs layer on top of federal benefits and can add thousands more in savings. Eligibility rules and amounts vary by province [1].

Provincial highlights

| Province | Program | Maximum Benefit |

|---|---|---|

| Ontario | Land Transfer Tax Rebate | Up to $4,000 |

| Toronto (City) | Municipal Land Transfer Tax Rebate | Up to $4,475 |

| Quebec | Provincial Tax Credit | Up to $1,400 |

| Montreal | New home grant | Up to $15,000 (new) / $7,000 (existing) |

| Prince Edward Island | Land Transfer Tax Rebate | Full rebate (homes ≤ $200,000) |

Ontario buyers can receive both the provincial and Toronto municipal rebates if purchasing in the city, for a combined maximum of $8,475 in land transfer tax relief [1].

If you’re weighing property types in Ontario, this comparison of condo versus house purchases in Ontario can help you decide which option aligns with your budget and eligibility for these rebates.

How Do Down Payment Requirements Affect First-Time Buyers?

Down payment rules are set federally and apply to all buyers, but understanding them is essential for planning which incentive programs to use [1].

Down payment minimums (2026)

- 5% for homes priced under $500,000

- 10% on the portion between $500,000 and $1.5 million

- 20% for homes priced above $1.5 million (no mortgage default insurance available)

Any down payment below 20% requires mortgage default insurance (through CMHC, Sagen, or Canada Guaranty). This adds a premium of 2.8% to 4% of the mortgage amount, depending on the down payment size.

Practical example: On a $700,000 home with 10% down ($70,000), the insured mortgage is $630,000. A 3.1% CMHC premium adds $19,530 to the mortgage, bringing the total to $649,530. The 30-year amortization option can help manage the monthly payment on this larger balance.

For information on why mortgage loan insurance exists and how it protects buyers, it’s worth understanding the role CMHC plays in making low-down-payment purchases possible.

How to Apply for First-Time Home Buyer Programs: Step-by-Step

Applying for multiple programs at once can feel overwhelming. Here’s a practical sequence that works for most buyers.

Step-by-step checklist

- Open an FHSA as early as possible (even if you’re 2-3 years from buying) — contribution room accumulates annually

- Check RRSP balances and confirm funds have been in the account for 90+ days before your planned withdrawal

- Get mortgage pre-approval and confirm eligibility for 30-year amortization if needed

- Confirm first-time buyer status — you must not have owned a home in the last four years for most programs

- Purchase a qualifying home — new builds qualify for the GST rebate; all qualifying homes qualify for the tax credit and RRSP plan

- Apply for the GST/HST rebate — your builder may credit it at closing, or you apply directly to the CRA within two years [2]

- Claim the Home Buyers’ Tax Credit on your tax return for the year of purchase

- Apply for provincial rebates — land transfer tax rebates are typically applied at closing through your lawyer

- Start RRSP repayments two years after the year of withdrawal (set a calendar reminder)

Common mistake: Forgetting to open an FHSA before the purchase year. You need to open the account and make at least one contribution before you can make a qualifying withdrawal. See our guide on common first-time home buyer mistakes to avoid other costly errors.

What Are the Pros and Cons of the Current First-Time Buyer Incentive Programs?

Pros

- No equity sharing: Unlike the old shared-equity incentive, current programs don’t give the government a stake in your home

- Stackable benefits: FHSA, RRSP HBP, tax credit, and GST rebate can all be used together

- Significant GST savings: Up to $50,000 back on a new home is a major cash benefit [6]

- Flexible savings: FHSA funds transfer to RRSP if unused, so there’s no downside to opening one early

- Lower monthly payments: 30-year amortization helps buyers in expensive markets qualify and manage cash flow

Cons

- RRSP repayment obligation: Missing HBP repayments adds income to your tax bill

- New builds only for GST rebate: Existing homes don’t qualify for the $50,000 GST benefit

- Income and price limits: Some provincial programs have income caps or maximum purchase prices

- Complexity: Managing multiple programs, deadlines, and repayment schedules requires careful planning

- Credit score impact: Poor credit can affect mortgage qualification regardless of incentive eligibility — see how to improve your credit score in Canada before applying

Frequently Asked Questions

Q: Is the original First-Time Home Buyer Incentive (shared-equity mortgage) still available?

No. The federal government officially ended the shared-equity First-Time Home Buyer Incentive in 2024. The programs described in this article are the current replacements.

Q: Can I use the FHSA and the RRSP Home Buyers’ Plan at the same time?

Yes. Both can be used for the same home purchase. A couple using both accounts could access up to $200,000 from registered savings ($40,000 FHSA + $60,000 RRSP per person).

Q: Does the GST/HST rebate apply to resale homes?

No. The First-Time Home Buyers’ GST/HST Rebate applies only to newly constructed or substantially renovated homes. Resale homes are generally exempt from GST/HST and therefore don’t qualify [6].

Q: How long do I have to apply for the GST/HST rebate?

Up to two years from the date you take ownership or complete construction of the home [2].

Q: What counts as “first-time buyer” for these programs?

For most federal programs, you must not have owned a home or lived in a spouse or common-law partner’s home as your primary residence at any point in the last four years [1].

Q: Can I use the Home Buyers’ Plan if I’ve used it before?

Yes, but only if you’ve fully repaid the previous withdrawal and meet the first-time buyer definition again (no home ownership in the past four years).

Q: What happens if I don’t repay my RRSP Home Buyers’ Plan withdrawal?

The amount you were supposed to repay in a given year is added to your taxable income for that year. Over time, this can result in a significant tax bill.

Q: Does the 30-year amortization cost more overall?

Yes. While monthly payments are lower, you pay more total interest over a 30-year term compared to 25 years. It’s a trade-off between monthly affordability and total cost.

Q: Can non-permanent residents use these programs?

Most programs require Canadian residency. Some require permanent residency or citizenship. Check with a mortgage broker or the CRA for your specific immigration status.

Q: Is there a maximum home price for the GST/HST rebate?

The rebate covers the full GST or federal portion of HST with no stated maximum home price, but the maximum rebate amount is capped at $50,000 [6].

Q: Are there programs specifically for new construction purchases?

Yes. The GST/HST rebate is the primary federal program for new construction. Some provinces and municipalities also offer additional grants for new builds, particularly in cities with housing supply goals.

Q: Should I work with a mortgage broker to access these programs?

A mortgage broker can help identify which programs you qualify for, structure your application, and connect you with lenders who offer 30-year amortization. It’s a practical first step for most buyers.

Conclusion

The first-time home buyer incentive landscape from the Government of Canada has changed significantly in 2026. The old shared-equity program is gone, replaced by a set of more direct and flexible tools: a GST rebate worth up to $50,000 on new homes, a powerful tax-free savings account (FHSA), an expanded RRSP withdrawal limit, a tax credit on closing costs, and access to 30-year mortgage amortization.

The key to maximizing these benefits is planning ahead and stacking programs strategically.

Actionable next steps

- Open an FHSA today if you plan to buy within the next 1-5 years — annual contribution room accumulates whether you use it or not

- Check your RRSP balance and confirm the 90-day holding rule for any funds you plan to withdraw

- Research provincial programs in your target market — Ontario, Quebec, and PEI all offer meaningful additional rebates

- If buying new construction, confirm with your builder whether they’ll credit the GST rebate at closing or if you’ll apply separately

- Speak with a mortgage broker to understand how your down payment, amortization choice, and stress test qualification interact

- Review your credit profile well before applying — improving your credit score can meaningfully affect the mortgage rate you qualify for

For buyers who are still saving, explore strategies to become mortgage-free faster once you’ve made your purchase.

References

[1] First Time Home Buyer Programs – https://www.ratehub.ca/first-time-home-buyer-programs

[2] First Time Buyers Can Save More On New Homes The First Time Home Buyers Gst Hst Rebate Is Available Now – https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2026/first-time-buyers-can-save-more-on-new-homes-the-first-time-home-buyers-gst-hst-rebate-is-available-now.html

[3] First Time Buyer Incentives Canada 2026 – https://ratefair.ca/first-time-buyer-incentives-canada-2026/

[4] First Time Homebuyer Incentives In Canada – https://blog.remax.ca/first-time-homebuyer-incentives-in-canada/

[5] Canada Lowering Costs For First Time Home Buyers Of Pre Construction Homes – https://www.sorbaralaw.com/resources/knowledge-centre/publication/canada-lowering-costs-for-first-time-home-buyers-of-pre-construction-homes

[6] What Rebate – https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/what-rebate.html

[7] Gst New Housing Rebate – https://www.wolterskluwer.com/en-ca/expert-insights/gst-new-housing-rebate

[8] First Time Homebuyers Can Now Save Up To 50000 On Taxes – https://www.gta-homes.com/real-insights/news/first-time-homebuyers-can-now-save-up-to-50000-on-taxes/

[9] Government Of Canada Programs To Support Homebuyers – https://www.cmhc-schl.gc.ca/consumers/home-buying/government-of-canada-programs-to-support-homebuyers

Tags: first-time home buyer incentive, government of canada housing programs, first home savings account, FHSA, RRSP home buyers plan, GST HST rebate new homes, first-time home buyers tax credit, 30-year amortization, CMHC mortgage insurance, Ontario land transfer tax rebate, Canadian housing programs 2026, down payment assistance Canada