25 Mar

Last updated: March 25, 2026

Quick Answer: The first-time home buyer RRSP strategy, formally called the Home Buyers Plan (HBP), lets eligible Canadians withdraw up to $60,000 from their RRSP tax-free to fund a home purchase. The withdrawn amount must be repaid to the RRSP over 15 years. Couples can combine withdrawals for up to $120,000 total. The HBP can also be used alongside the newer First Home Savings Account (FHSA) for an even larger down payment.

Key Takeaways

- Maximum withdrawal: $60,000 per person ($120,000 per couple) from an RRSP under the Home Buyers Plan [1][4]

- Repayment window: 15 years, with at least 1/15 of the total repaid each year [2]

- No tax on withdrawal — as long as repayment rules are followed; missed repayments are added to taxable income

- Funds must sit in the RRSP for at least 90 days before withdrawal or they won’t qualify

- A written purchase or build agreement is required — a mortgage pre-approval alone does not qualify [1]

- The home must be your principal residence within one year of acquisition [1]

- Extended grace period applies to withdrawals made between January 1, 2022 and December 31, 2025 — repayment can start up to 5 years after withdrawal [1]

- The FHSA is often a stronger first option — no repayment required — but both accounts can be used together [1][4]

- 2026 RRSP contribution room is $33,810, up from $32,490 in 2025 [3]

- “First-time buyer” has a specific CRA definition — previous homeowners may still qualify after a four-year gap [1]

What Is the First-Time Home Buyer RRSP Program (Home Buyers Plan)?

The Home Buyers Plan (HBP) is a federal Canadian program that allows first-time home buyers to withdraw money from their Registered Retirement Savings Plan (RRSP) without paying tax on it at the time of withdrawal — provided the funds are repaid over time. It was designed to help Canadians bridge the gap between their savings and the down payment needed to buy a home.

As of April 16, 2024, the withdrawal limit increased from $35,000 to $60,000 per person, a significant change that reflects rising home prices across Canada [4]. For couples buying together, this means a combined maximum of $120,000 can be pulled from their respective RRSPs for the same purchase [2].

The key distinction from a regular RRSP withdrawal: the HBP is structured as an interest-free loan to yourself. The money leaves the RRSP, goes toward your home purchase, and then gets repaid back into the RRSP over 15 years. If you don’t repay in a given year, that year’s required repayment amount gets added to your taxable income — which effectively means you pay income tax on it.

Who Qualifies as a First-Time Home Buyer for the RRSP HBP?

The CRA’s definition of “first-time home buyer” is more flexible than most people assume — previous homeowners can still qualify.

You qualify as a first-time buyer if:

- You have not owned a qualifying home that you occupied as your principal residence at any time during the current calendar year (except in the 30 days immediately before the withdrawal date) or in any of the four preceding calendar years [1]

Practical example: If you owned and lived in a home but sold it in 2021 and have rented since, you would qualify again for the HBP as of January 1, 2026.

Disability exception: Canadians with a disability (or those helping a related person with a disability) can use the HBP even if they don’t meet the first-time buyer rule, provided the home better suits the person’s needs.

Additional eligibility requirements:

- Must be a Canadian resident at the time of withdrawal and through the required CRA-specified periods

- Must have a written agreement to buy or build a qualifying home — a mortgage pre-approval does not count [1]

- Must intend to occupy the home as your principal residence within one year of acquisition or construction [1]

- The home must be acquired or built before October 1 of the year following the year of your first HBP withdrawal [1]

⚠️ Common mistake: Many buyers assume a mortgage pre-approval satisfies the HBP eligibility requirement. It does not. A signed purchase agreement or build contract is mandatory before withdrawing.

How Does the First-Time Home Buyer RRSP Withdrawal Process Work?

The HBP withdrawal process is straightforward, but the order of steps matters. Skipping or reversing steps can disqualify your withdrawal.

Step-by-step process:

- Confirm eligibility — verify you meet the first-time buyer definition and residency requirements

- Sign a purchase or build agreement — this must exist before you withdraw

- Ensure funds have been in the RRSP for 90+ days — contributions made within 90 days of withdrawal do not count toward the HBP [4]

- Complete CRA Form T1036 (Home Buyers’ Plan Request to Withdraw Funds from an RRSP) — submit this to your RRSP issuer

- Receive the funds — your financial institution processes the withdrawal without withholding tax

- Use funds for the home purchase — apply toward your down payment or closing costs

- File your tax return — report the HBP withdrawal on Schedule 7 of your T1 return

- Begin repayments — contributions to your RRSP designated as HBP repayments start in the applicable year

The 90-day rule is critical. If someone contributes $20,000 to their RRSP in February and tries to withdraw it under the HBP in April of the same year, that $20,000 won’t qualify. Only funds held for at least 90 days are eligible.

What Are the Repayment Rules for the RRSP Home Buyers Plan?

Once you’ve used the HBP, repayment begins based on the year of your withdrawal — and the rules changed recently for those who withdrew during the pandemic years.

Standard repayment timeline:

- Repayment generally begins two years after the calendar year of withdrawal

- The repayment period spans 15 years [2]

- Each year, you must repay at least 1/15 of the total amount withdrawn [2]

- Repayments are made as RRSP contributions designated on your tax return

Extended grace period (2022–2025 withdrawals):

For withdrawals made between January 1, 2022 and December 31, 2025, the federal government extended the repayment start date by an additional three years. This means repayment can be deferred for up to five years from the year of withdrawal [1].

| Withdrawal Year | Standard Repayment Start | Extended Repayment Start |

|---|---|---|

| 2022 | 2024 | 2027 |

| 2023 | 2025 | 2028 |

| 2024 | 2026 | 2029 |

| 2025 | 2027 | 2030 |

What happens if you miss a repayment?

The required repayment amount for that year is added to your taxable income. You don’t lose the HBP, but you’ll pay income tax on whatever portion you didn’t repay — effectively undoing the tax-deferral benefit for that amount.

💡 Pro tip: Set up automatic annual RRSP contributions specifically designated as HBP repayments. This prevents accidental missed repayments and keeps your retirement savings on track.

How Much Can You Withdraw, and How Does It Compare to Other Programs?

The first-time home buyer RRSP program now offers the highest single-account withdrawal limit among federal homebuying assistance programs — but it comes with a repayment obligation that other programs don’t.

HBP withdrawal limits:

- Individual: Up to $60,000 [4]

- Couple (two eligible buyers): Up to $120,000 combined [2]

- Minimum RRSP balance required: No minimum, but only funds held 90+ days qualify

2026 RRSP contribution room: $33,810 (18% of earned income, up to this maximum) [3]. This means a disciplined saver contributing the maximum for two years could accumulate enough for a significant HBP withdrawal.

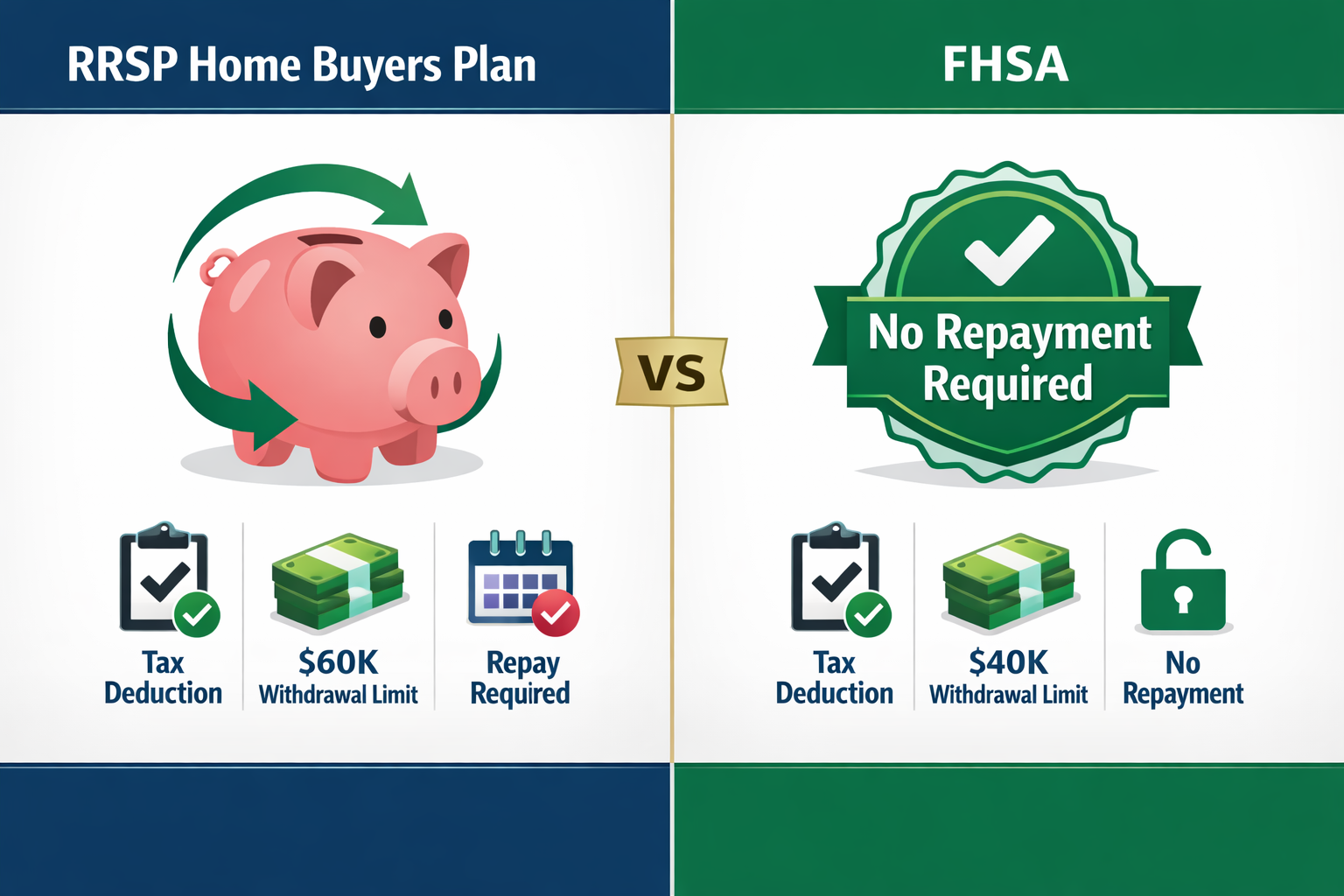

HBP vs. FHSA: Which Is Better for First-Time Buyers?

The First Home Savings Account (FHSA), introduced in 2023, is often recommended as the stronger option for first-time buyers who haven’t purchased yet — but the two accounts can be used together [1][4].

| Feature | RRSP (HBP) | FHSA |

|---|---|---|

| Max withdrawal | $60,000 | $40,000 lifetime |

| Tax on contribution | Deductible (already done) | Deductible |

| Tax on withdrawal | None (if repaid) | None (no repayment needed) |

| Repayment required | Yes — 15 years | No |

| Annual contribution limit | $33,810 (2026) | $8,000/year |

| Unused room carries forward | Yes | Yes (up to $8,000) |

| Can combine with the other | Yes | Yes |

Choose the FHSA first if you haven’t opened one yet and have time to contribute — the tax-free withdrawal with no repayment obligation is a clear advantage. Use the HBP to supplement when you need more than the FHSA can provide, or if your RRSP already holds substantial funds. Using both together for the same purchase is permitted [4].

For a broader look at programs available to first-time buyers, see this overview of the first-time home buyers incentive program.

What Are the Pros and Cons of Using Your RRSP as a First-Time Home Buyer?

The HBP is a useful tool, but it’s not the right move for everyone. Understanding the trade-offs helps you decide whether to use it, how much to withdraw, and whether to combine it with other strategies.

Pros:

- Access a large lump sum (up to $60,000) without immediate tax consequences

- Couples can combine for up to $120,000 — a meaningful down payment in most Canadian markets

- No interest charged on the “loan” from your RRSP

- Can be combined with FHSA withdrawals for even greater purchasing power

- Extended grace period for 2022–2025 withdrawals gives more breathing room

Cons:

- Withdrawn funds lose years of tax-sheltered compound growth — this is the real cost

- Repayment obligation lasts 15 years; missed payments become taxable income

- Only funds held 90+ days qualify — last-minute RRSP top-ups don’t count

- Reduces your retirement savings base, which may be hard to rebuild

- FHSA is often a better first option since there’s no repayment required

Edge case — early repayment: You can repay the full HBP balance early with no penalty. If your income increases significantly after buying, making accelerated repayments is a smart way to restore your RRSP’s growth potential faster.

To avoid common pitfalls in the homebuying process, review this guide on first-time home buyer mistakes before making any major decisions.

How Does the Mortgage Stress Test Interact With Your RRSP Down Payment?

A larger down payment from your RRSP HBP withdrawal directly affects your mortgage qualification — and can reduce the impact of the stress test.

The mortgage stress test requires Canadian borrowers to qualify at either 5.25% or the contract rate plus 2%, whichever is higher [see the full breakdown in this guide on the mortgage stress test for home buyers]. A larger down payment means a smaller mortgage, which means the stress test threshold is easier to clear on a lower loan amount.

Practical impact of a $60,000 HBP withdrawal:

- On a $600,000 home, a $60,000 down payment (10%) vs. a $120,000 down payment (20%) changes both the mortgage insurance requirement and the monthly payment significantly

- Reaching 20% down eliminates the need for CMHC mortgage default insurance, saving thousands over the life of the mortgage

If you’re comparing property types and how down payment size affects your purchase, this guide on condo versus house purchases in Ontario is worth reading before you commit.

What Strategies Maximize the First-Time Home Buyer RRSP Benefit?

The HBP works best when it’s part of a deliberate savings plan — not a last-minute scramble. Here are the strategies that produce the best outcomes.

Strategy 1: Contribute to RRSP early, then withdraw Contribute to your RRSP well before you plan to buy (at least 90 days, ideally longer). You get the tax deduction on contributions, your refund can be reinvested, and then you withdraw under the HBP. This effectively gives you a tax refund “boost” before your purchase.

Strategy 2: Use FHSA first, HBP second Max out your FHSA contributions each year ($8,000/year, up to $40,000 lifetime). When you’re ready to buy, withdraw from the FHSA first (no repayment), then use the HBP for any remaining gap. This minimizes your repayment obligation.

Strategy 3: Couples should each open separate RRSPs Both partners need their own RRSP with qualifying funds to access the full $120,000 combined limit. Spousal RRSPs can be part of this strategy, but attribution rules apply — contributions made within three calendar years before withdrawal may be attributed back to the contributing spouse.

Strategy 4: Plan repayments around income peaks If you expect your income to rise in future years, making larger HBP repayments in those years reduces taxable income more efficiently. Conversely, in lower-income years, it may be acceptable to let a small portion become taxable income if the marginal rate is low.

For long-term financial planning beyond the purchase, these saving tips to become mortgage-free offer practical strategies to accelerate your path to full ownership.

Frequently Asked Questions

Q: Can I use the HBP if I’ve owned a home before? Yes — if you haven’t owned a qualifying home that you occupied as your principal residence in the current year (except within 30 days of withdrawal) or in the previous four calendar years, you qualify again. [1]

Q: What happens to my HBP if I die or become a non-resident? If you become a non-resident of Canada, the full outstanding HBP balance must be repaid by the end of the year following the year you became a non-resident, or it becomes fully taxable. In the event of death, the balance is included in the deceased’s income for that tax year unless a surviving spouse assumes the balance.

Q: Can I use the HBP for a rental property? No. The home must be your principal residence. It cannot be used for a property you intend to rent out without occupying yourself.

Q: Does my RRSP need a minimum balance before I can use the HBP? No minimum balance is required, but only funds held for at least 90 days qualify. You can make multiple withdrawals across different RRSP accounts, as long as the total doesn’t exceed $60,000 and each account’s funds meet the 90-day rule. [4]

Q: Can I use the HBP and the FHSA for the same home purchase? Yes. Both can be used for the same qualifying home purchase, allowing buyers to combine withdrawal sources for a larger down payment. [4]

Q: What if my home purchase falls through after I’ve withdrawn from my RRSP? If the purchase doesn’t proceed, you generally have until October 1 of the year following the withdrawal to either acquire a qualifying home or repay the full amount to your RRSP. If neither happens, the full withdrawal becomes taxable income. [1]

Q: Is the HBP available for new construction? Yes — the HBP can be used to build a qualifying home, not just purchase an existing one. The home must be substantially complete before October 1 of the year following your first withdrawal. [1]

Q: How do I designate RRSP contributions as HBP repayments? On your annual T1 tax return, use Schedule 7 to designate RRSP contributions as HBP repayments. Simply contributing to your RRSP does not automatically count as a repayment — you must designate it.

Q: What is the 2026 RRSP contribution limit? The 2026 RRSP contribution limit is $33,810, representing 18% of earned income up to that maximum. [3]

Q: Can I withdraw from a spousal RRSP under the HBP? Yes, but the annuitant (the person whose name is on the RRSP) must be the one making the withdrawal. Attribution rules may apply if contributions were made within the previous three calendar years.

Q: What if I can’t afford to repay the HBP in a given year? The required annual repayment (1/15 of total withdrawn) is added to your taxable income for that year. You don’t lose access to the HBP, but you lose the tax-deferral benefit on that amount. [2]

Q: Is there a penalty for repaying the HBP early? No. You can repay the full balance at any time with no penalty, which restores your RRSP’s growth potential sooner.

Conclusion

The first-time home buyer RRSP program remains one of the most accessible tools available to Canadians saving for a down payment. With the 2024 increase to $60,000 per person — and up to $120,000 for couples — the Home Buyers Plan can make a meaningful difference in reaching the down payment threshold, especially in higher-cost markets.

That said, the HBP works best when used strategically, not reactively. The 90-day rule, the written agreement requirement, and the 15-year repayment obligation all require planning ahead. And for buyers who haven’t yet purchased, opening and maximizing an FHSA first — then supplementing with the HBP — is typically the more efficient approach, since FHSA withdrawals carry no repayment obligation.

Actionable next steps for 2026:

- Check your RRSP balance and contribution history — confirm which funds have been held for 90+ days

- Open an FHSA if you haven’t already — contribute up to $8,000 this year and carry forward unused room

- Get a signed purchase or build agreement before initiating any HBP withdrawal

- Complete CRA Form T1036 and submit to your RRSP issuer

- Plan your 15-year repayment schedule — set calendar reminders and automate contributions where possible

- Consult a mortgage professional to understand how your down payment size affects your mortgage qualification and stress test results

For personalized guidance on how the HBP fits into your overall mortgage strategy, speaking with a licensed mortgage professional is the most reliable next step.

References

[1] RRSP First Time Home Buyers Plan Strategy – https://pragmatic.mortgage/hub/rrsp-first-time-home-buyers-plan-strategy

[2] How Will The Home Buyers Plan Changes Affect Me – https://www.affinitycu.ca/investing/tools-and-resources/advice/how-will-the-home-buyers-plan-changes-affect-me

[3] Parallel Wealth — 2026 RRSP Contribution Limit Overview – https://www.youtube.com/watch?v=DupyxRVS2VI

[4] What Home Buyers Plan – https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan.html

Tags: first-time home buyer RRSP, Home Buyers Plan, HBP withdrawal, RRSP down payment, FHSA vs RRSP, Canadian mortgage tips, RRSP repayment rules, first-time buyer Canada, down payment strategies, CMHC mortgage, RRSP contribution limit 2026, CRA Form T1036