Last updated: March 25, 2026

Quick Answer: A first-time home buyer savings account is a tax-advantaged account that lets eligible buyers set aside money specifically for a home purchase. In Canada, the First Home Savings Account (FHSA) is already law, offering up to $40,000 in lifetime tax-free contributions. In the U.S., several legislative proposals introduced in 2026 would create similar dedicated savings vehicles, though none have been signed into law yet.

Key Takeaways

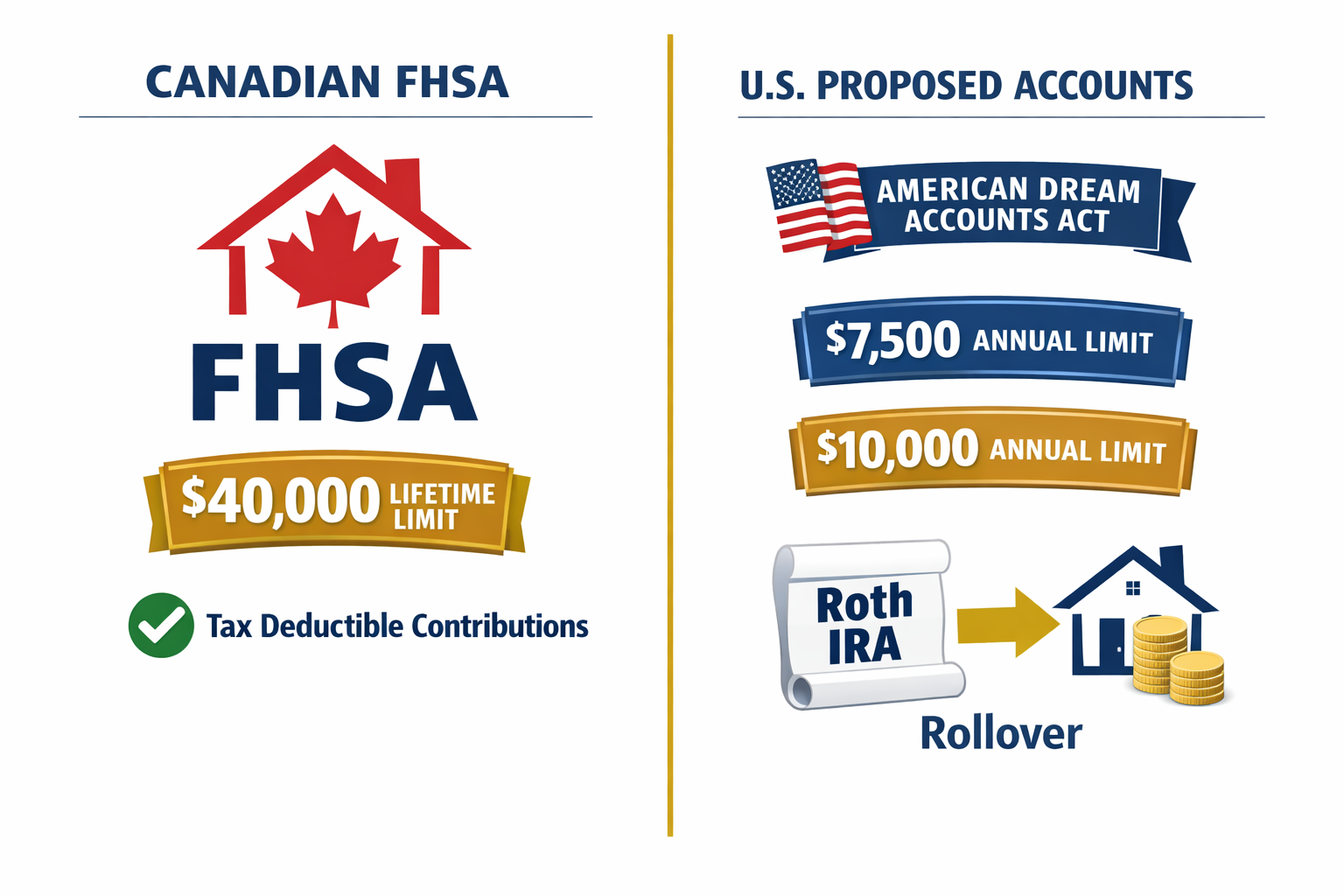

- 🏠 Canada's FHSA lets first-time buyers contribute up to $8,000 per year (lifetime max $40,000) with tax-deductible contributions and tax-free withdrawals for a qualifying home purchase.

- 💡 In the U.S., the American Dream Accounts Act (introduced March 2026) proposes annual limits of $7,500 (under 35) or $10,000 (35+), with a $250,000 lifetime cap per account holder [2].

- 📋 Multiple U.S. bills — including the First Home Savings Opportunity Act and the NEST Act — are competing to define what a first-time home buyer savings account looks like at the federal level [4][6].

- 🔄 Unused U.S. American Dream Account funds (up to $100,000) could roll over to a Roth IRA or a family member's account under the proposed legislation [2].

- ⚠️ A 10% penalty applies to non-qualifying withdrawals under the American Dream Accounts Act proposal, and homes purchased with account funds must be held for at least three years to avoid taxation [2].

- 🇨🇦 Canadian FHSA contributions are tax-deductible (like an RRSP), and qualifying withdrawals are tax-free (like a TFSA) — a rare double tax benefit.

- 📅 The U.S. American Dream Accounts Act, if enacted, would apply to taxable years beginning after December 31, 2026 [2].

- 🏦 State-level programs (like New Jersey's S-1756) are already filling the gap where federal legislation hasn't passed, with annual limits up to $15,000 and lifetime caps of $75,000 [1].

- 🔍 Combining a first-time home buyer savings account with other programs (RRSP Home Buyers' Plan in Canada, or IRA withdrawals in the U.S.) can significantly accelerate a down payment.

What Is a First-Time Home Buyer Savings Account?

A first-time home buyer savings account is a dedicated, tax-advantaged account designed to help people save specifically for their first home purchase. Unlike a general savings account, these accounts offer tax benefits — such as deductible contributions, tax-free growth, or tax-free withdrawals — that make it faster and more efficient to build a down payment.

The exact structure depends on the country or state. Canada's version (the FHSA) is already active. In the United States, the concept exists in several proposed forms at both the federal and state levels, but no single national standard has been enacted as of early 2026.

Who qualifies as a "first-time buyer" in most programs:

- Has not owned a qualifying home in the current year or the preceding four calendar years (Canada's definition)

- Has not owned a principal residence in the past three years (common U.S. definition)

- Plans to use the funds for a down payment or eligible closing costs on a primary residence

"A dedicated savings account for a first home isn't just a savings tool — it's a tax strategy that can shave years off the time it takes to reach a down payment goal."

How Does Canada's First Home Savings Account (FHSA) Work?

Canada's FHSA, launched in 2023, is the most fully developed first-time home buyer savings account program in North America. It combines the best features of two existing account types: the RRSP (tax-deductible contributions) and the TFSA (tax-free withdrawals).

Core FHSA rules at a glance:

| Feature | Detail |

|---|---|

| Annual contribution limit | $8,000 |

| Lifetime contribution limit | $40,000 |

| Contribution tax treatment | Deductible from income |

| Investment growth | Tax-free |

| Qualifying withdrawal | Tax-free |

| Non-qualifying withdrawal | Taxable as income |

| Account lifespan | 15 years (or until age 71) |

| Unused room carryforward | Up to $8,000 per year |

For a deeper look at how the FHSA works in practice, see this introduction to the First Home Savings Account (FHSA) and the guide on how the tax-free First Home Savings Account can help you buy a house.

Common mistake: Opening an FHSA and not investing the funds. Leaving contributions in cash means missing out on tax-free investment growth — the account works best when contributions are invested in eligible securities like mutual funds or ETFs.

Edge case: If you never buy a home, you can transfer the FHSA balance to an RRSP without tax consequences, so the money isn't lost.

What U.S. Legislation Proposes for a First-Time Home Buyer Savings Account?

Several U.S. bills introduced in 2025 and 2026 propose creating a dedicated first-time home buyer savings account at the federal level. None are law yet, but the legislative momentum is notable.

American Dream Accounts Act (2026)

Introduced by Senator Rick Scott in March 2026, this bill would create a new tax-advantaged account specifically for first-time buyers [2][5].

Key proposed features:

- Annual contribution limits: $7,500 for account holders under age 35; $10,000 for those 35 and older [2]

- Lifetime contribution cap: $250,000 per account holder [2]

- Maximum eligible distribution: Up to $500,000 for a single buyer, or $250,000 per person for joint purchasers [2]

- 3-year holding rule: If the home is sold within three years of purchase, the withdrawn amount becomes taxable. Exceptions apply for military service, death, divorce, and job loss [2]

- Non-qualifying withdrawal penalty: 10% on funds used for purposes other than a first home purchase [2]

- Rollover option: Up to $100,000 in unused funds can transfer to a Roth IRA or a family member's American Dream Account [2]

- Effective date (if enacted): Taxable years beginning after December 31, 2026 [2]

First Home Savings Opportunity Act

Introduced by Representatives Suhas Subramanyam (VA-10) and Ashley Hinson (IA-02), this bipartisan bill would allow annual contributions of up to $10,000 ($20,000 for joint filers) to a tax-deductible savings account for down payments and closing costs [4].

First Time Homeowner Savings Plan Act (H.R. 2748)

This bill raises the existing IRA penalty-free withdrawal limit for first-time buyers from $10,000 to $25,000, with annual inflation adjustments beginning in 2027 [3]. It doesn't create a new account type — instead, it expands access to existing IRA funds.

NEST Act (H.R. 7422)

The Next-Generation Equity Savings Tool Act, introduced by Representatives Kat Cammack and Jim Moylan, ties contribution deduction limits to 20% of median home sale prices in the account holder's state, with annual adjustments [6]. This approach acknowledges that housing costs vary dramatically by region.

Decision rule: If you're a U.S. buyer planning ahead, the most practical step right now is to use a high-yield savings account or Roth IRA (up to existing limits) while monitoring which of these bills advances. Don't delay saving while waiting for legislation to pass.

What State-Level First-Time Home Buyer Savings Accounts Are Available?

Several U.S. states have already enacted their own first-time home buyer savings account programs, independent of federal legislation.

New Jersey (S-1756): This legislation establishes special savings accounts certified by the New Jersey Housing and Mortgage Finance Agency. Key terms include annual contributions up to $15,000 and a lifetime cap of $75,000 [1]. Funds can be used for down payments and eligible closing costs on a primary residence in New Jersey.

Other states with similar programs (as of 2026) include:

- Minnesota — First-Time Homebuyer Savings Account with state income tax deductions

- Montana — First-Time Home Buyer Savings Account program

- Mississippi — First-Time Home Buyer Savings Account with state deduction

- Virginia — Home Purchase Assistance savings account provisions

Important note: State programs vary widely in contribution limits, eligible uses, and whether funds must be used in-state. Always verify current rules with your state's housing finance agency, as program details can change annually.

How Does a First-Time Home Buyer Savings Account Compare to Other Savings Options?

A first-time home buyer savings account isn't the only way to save for a down payment. Understanding how it stacks up against alternatives helps buyers choose the right combination.

| Account Type | Tax Deduction on Contribution | Tax-Free Growth | Tax-Free Withdrawal | Penalty for Non-Home Use |

|---|---|---|---|---|

| FHSA (Canada) | ✅ Yes | ✅ Yes | ✅ Yes (qualifying) | ❌ Taxable as income |

| TFSA (Canada) | ❌ No | ✅ Yes | ✅ Yes (any purpose) | None |

| RRSP Home Buyers' Plan | ✅ Yes (on contribution) | ✅ Yes | ✅ Yes (must repay) | Must repay over 15 years |

| Roth IRA (U.S.) | ❌ No | ✅ Yes | ✅ Yes (after 5 yrs) | 10% on earnings (exceptions apply) |

| American Dream Account (proposed U.S.) | ✅ Yes (proposed) | ✅ Yes (proposed) | ✅ Yes (qualifying) | 10% penalty [2] |

| High-Yield Savings Account | ❌ No | ❌ No (interest taxable) | ✅ Yes | None |

For Canadian buyers deciding between account types, the TFSA vs. FHSA comparison is worth reading before opening any new account.

Choose the FHSA if: You're a Canadian first-time buyer who wants both a tax deduction now and a tax-free withdrawal later.

Choose the TFSA if: You want flexibility — the funds can be used for anything, not just a home.

Use both if: You can afford to maximize contributions to each. Many buyers pair an FHSA with the RRSP Home Buyers' Plan for maximum down payment savings.

How Do You Open and Use a First-Time Home Buyer Savings Account?

Opening a first-time home buyer savings account is straightforward in Canada. In the U.S., the process depends on which state program (if any) applies to you.

Steps for Canadian Buyers (FHSA)

- Confirm eligibility: You must be a Canadian resident, at least 18 years old, and a first-time home buyer (no owned qualifying home in the current year or the prior four years).

- Choose a financial institution: Most major banks, credit unions, and online brokerages offer FHSAs.

- Open the account: Bring government-issued ID. The process is similar to opening a TFSA.

- Choose your investments: Eligible investments include GICs, mutual funds, ETFs, and stocks. Don't leave the money in cash.

- Contribute up to $8,000 per year: Unused room from the prior year carries forward (max $8,000 carryforward).

- Claim the deduction: Report FHSA contributions on your annual tax return to reduce taxable income.

- Make a qualifying withdrawal: When you're ready to buy, submit a completed Form RC725 to your financial institution to withdraw funds tax-free.

Steps for U.S. Buyers (State Programs)

- Check your state's housing finance agency website for an active first-time home buyer savings account program.

- Open a designated account at a participating bank or credit union (requirements vary by state).

- Keep records of contributions and withdrawals — most state programs require documentation to claim the deduction.

- Use funds only for eligible purposes (down payment, closing costs on a primary residence in-state, in most cases).

For a broader view of the home-buying process, the complete guide to saving and buying your first home covers the full timeline from saving to closing.

What Are the Biggest Mistakes Buyers Make With These Accounts?

Most mistakes with a first-time home buyer savings account fall into a few predictable categories.

1. Opening the account too late

The FHSA's 15-year lifespan and $8,000 annual limit mean the sooner you open it, the more room you accumulate. Waiting until you're actively house-hunting costs contribution room you can't recover.

2. Not investing contributions

Leaving FHSA or state savings account funds in cash earns minimal interest and misses the compounding benefit of invested assets over several years.

3. Mixing up eligibility rules

The "first-time buyer" definition differs between programs. Someone who owned a home five years ago may qualify under one program but not another. Verify before contributing.

4. Withdrawing for non-qualifying purposes

A 10% penalty applies to non-qualifying withdrawals under proposed U.S. legislation [2]. In Canada, non-qualifying FHSA withdrawals are fully taxable as income. Always confirm the purpose qualifies before withdrawing.

5. Ignoring other available programs

A first-time home buyer savings account works best alongside other programs. Canadian buyers should also explore the First-Time Home Buyer Tax Credit and the First-Time Home Buyers' Incentive program.

For a full list of common pitfalls, see this guide on first-time home buyer mistakes.

How Much Can a First-Time Home Buyer Savings Account Actually Help?

The tax savings from a dedicated first-time home buyer savings account can be significant, especially when contributions are invested over several years.

Example scenario (Canada, FHSA):

Assume a buyer in a 40% marginal tax bracket contributes $8,000 per year for five years:

- Total contributions: $40,000

- Tax refunds received (estimated at 40%): approximately $16,000

- Investment growth (assumed 5% annual return, tax-free): approximately $4,500

- Effective down payment boost vs. a regular savings account: roughly $20,500 ahead

This is an illustrative estimate based on assumed tax rate and return. Actual results depend on individual tax situations and investment performance.

For U.S. buyers under proposed legislation:

A 35-year-old contributing $10,000 per year for 10 years under the American Dream Accounts Act could accumulate up to $100,000 in contributions alone (within the $250,000 lifetime cap), with tax-deferred or tax-free growth on top [2]. The actual benefit depends on the final tax treatment written into law.

FAQ: First-Time Home Buyer Savings Account

Q: Can I have both an FHSA and a TFSA at the same time in Canada?

Yes. These are separate accounts with separate contribution limits. Many buyers maximize both to accelerate their down payment savings.

Q: What happens to my FHSA if I never buy a home?

In Canada, you can transfer the balance to an RRSP or RRIF without tax consequences, and without affecting your RRSP contribution room. The account must be closed by the end of the year you turn 71 or after 15 years, whichever comes first.

Q: Is the American Dream Accounts Act already law in the U.S.?

No. As of March 2026, it is a legislative proposal introduced by Senator Rick Scott. It has not been passed or signed into law [2].

Q: Can two people buying a home together both use their first-time home buyer savings accounts?

Yes. In Canada, both buyers can each use their own FHSA (up to $40,000 each). Under the proposed U.S. American Dream Accounts Act, joint purchasers could each access up to $250,000 in eligible distributions [2].

Q: Does the FHSA affect my RRSP Home Buyers' Plan eligibility?

No. Canadian buyers can use both the FHSA and the RRSP Home Buyers' Plan (up to $35,000 from an RRSP) for the same home purchase, effectively doubling their tax-advantaged down payment sources.

Q: What counts as an eligible home purchase under these programs?

Generally, the home must be a qualifying principal residence (not a rental or vacation property) that the buyer intends to occupy. Condos, detached houses, and semi-detached homes typically qualify. Confirm with your financial institution or program administrator.

Q: Are there income limits to open a first-time home buyer savings account?

Canada's FHSA has no income limits. U.S. proposed legislation (as of 2026) does not specify income limits, though final bill text could change this.

Q: What if I contribute more than the annual limit?

Excess FHSA contributions in Canada are subject to a 1% per month tax on the excess amount, similar to RRSP over-contribution penalties. Avoid contributing more than your available room.

Q: Can I use a first-time home buyer savings account for closing costs?

In Canada, FHSA withdrawals must be for a qualifying home purchase — closing costs are not explicitly covered as a standalone use, but the funds go toward the overall purchase. Some U.S. state programs and proposed federal bills explicitly include closing costs as an eligible expense [4].

Q: How does a first-time home buyer savings account interact with the mortgage stress test?

The savings account itself doesn't change the stress test calculation, but a larger down payment (20% or more) eliminates the need for mortgage default insurance and may improve your mortgage terms. See the mortgage stress test guide for details.

Q: What is the New Jersey first-time home buyer savings account program?

New Jersey's S-1756 establishes savings accounts certified by the NJ Housing and Mortgage Finance Agency, with annual contributions up to $15,000 and a lifetime cap of $75,000 [1]. Funds are intended for down payments and eligible costs on a New Jersey primary residence.

Q: Should I open a first-time home buyer savings account even if I'm not sure I'll buy?

In Canada, yes — because unused FHSA funds can roll into an RRSP tax-free, there's very little downside to opening one early. In U.S. states with active programs, review the penalty for non-qualifying withdrawals before committing.

Conclusion: Actionable Next Steps

A first-time home buyer savings account is one of the most efficient tools available for building a down payment — whether you're in Canada using the established FHSA or in the U.S. watching federal legislation take shape in 2026.

Here's what to do now:

- Canadian buyers: Open an FHSA immediately if you haven't. Contribute as much as you can (up to $8,000) before the tax year ends to start accumulating room and claim your deduction.

- U.S. buyers: Check your state's housing finance agency for an active state-level program. If none exists, use a Roth IRA or high-yield savings account while monitoring federal legislation.

- Combine programs: Don't rely on one account alone. Stack your FHSA with the RRSP Home Buyers' Plan (Canada) or a Roth IRA with the existing $10,000 penalty-free withdrawal (U.S.) to maximize your down payment.

- Invest your contributions: Leaving funds in cash wastes the tax-free growth benefit. Choose low-cost index funds or GICs appropriate for your timeline.

- Track your timeline: If buying within 1–2 years, keep investments conservative. If 3–5 years out, a growth-oriented portfolio within the account makes sense.

- Work with a mortgage professional: Understanding how your savings account interacts with mortgage qualification, the stress test, and available government programs can save you thousands. A qualified mortgage broker can map out the full picture.

The path to homeownership is long for many buyers, but a dedicated savings account — used strategically — can meaningfully shorten that timeline.

References

[1] Civicalerts – https://www.njsendems.org/CivicAlerts.aspx?AID=1231

[2] New Legislation Proposal Will Benefit First Time Buyers Relieving Some Affordability Pressures – https://themortgagepoint.com/2026/03/19/new-legislation-proposal-will-benefit-first-time-buyers-relieving-some-affordability-pressures/

[3] First Time Homeowner Savings Plan Act – https://homebuyer.com/congress/first-time-homeowner-savings-plan-act

[4] Rep Subramanyam Introduces Bipartisan Bill Help First Time Homebuyers Save – http://subramanyam.house.gov/media/press-releases/rep-subramanyam-introduces-bipartisan-bill-help-first-time-homebuyers-save

[5] Senator Unveils Tax Free Savings Plan Rescue American Dream From Soaring Home Costs – https://www.foxbusiness.com/politics/senator-unveils-tax-free-savings-plan-rescue-american-dream-from-soaring-home-costs

[6] First Time Homebuyer Accounts Proposed – https://www.ascensus.com/industry-regulatory-news/news-articles/first-time-homebuyer-accounts-proposed/

Tags: first-time home buyer savings account, FHSA Canada, American Dream Accounts Act, first home savings account, down payment savings, tax-free savings, home buyer programs 2026, RRSP Home Buyers Plan, TFSA vs FHSA, first-time buyer tax benefits, state home buyer savings accounts, mortgage down payment