Last updated: March 25, 2026

Quick Answer: First time home buyers in Ontario can access several federal and provincial programs that reduce upfront costs, including the First Home Savings Account (up to $40,000 tax-free), the Home Buyers' Plan (up to $60,000 from an RRSP), and land transfer tax rebates worth up to $4,000 provincially (plus $4,475 in Toronto). A minimum 5% down payment is required for homes priced up to $500,000, and buyers must pass the federal mortgage stress test. Stacking multiple programs together is the most effective way to reduce out-of-pocket costs.

Key Takeaways

- First time home buyers in Ontario can combine multiple programs to significantly reduce upfront costs — stacking is allowed and encouraged.

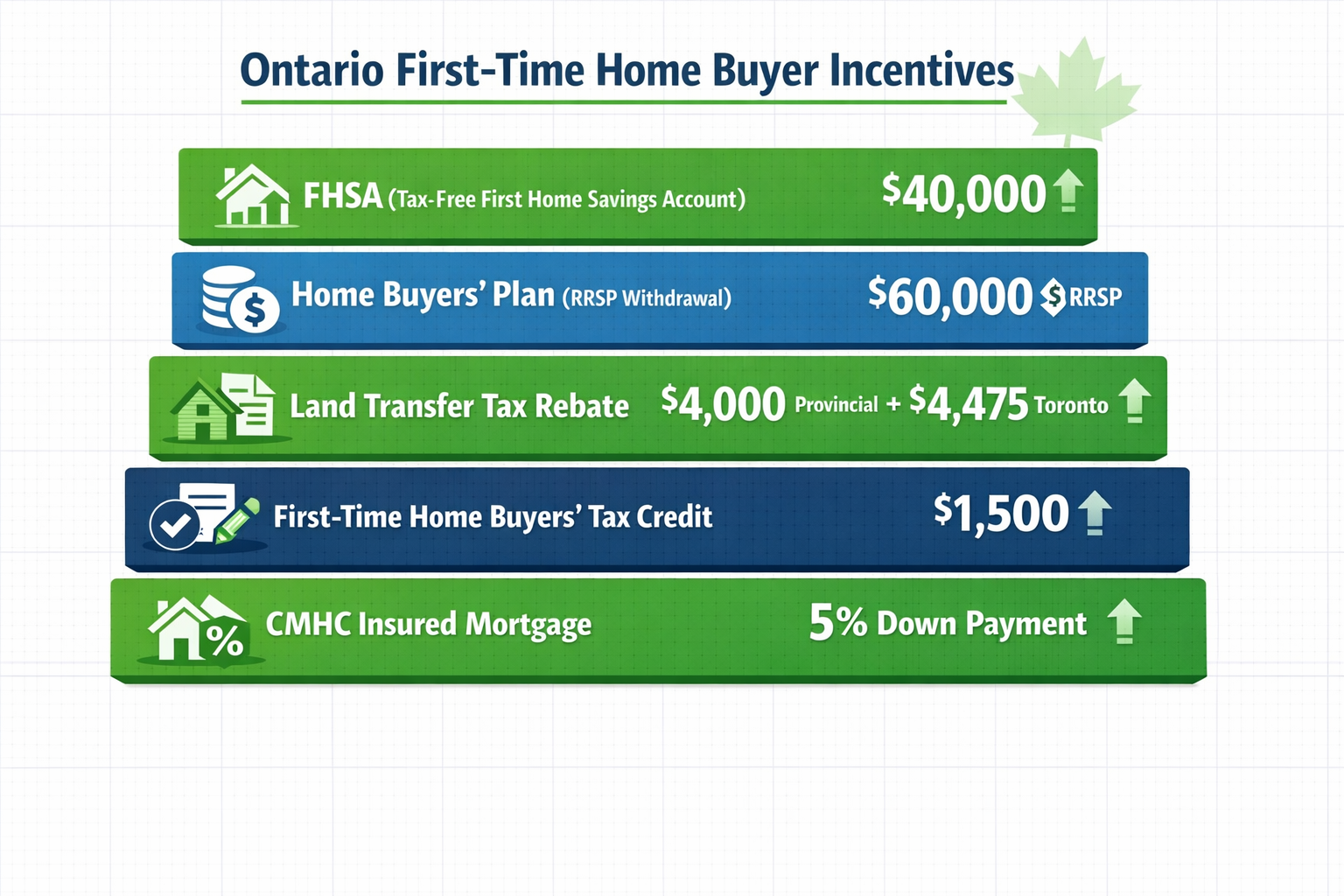

- The First Home Savings Account (FHSA) lets eligible buyers save up to $40,000 tax-free, with annual contribution room of $8,000. [2]

- The Home Buyers' Plan (HBP) allows withdrawing up to $60,000 per person from an RRSP, repayable over 15 years. [2]

- Ontario's provincial land transfer tax rebate covers up to $4,000; Toronto buyers get an additional municipal rebate of up to $4,475. [3]

- The First-Time Home Buyers' Tax Credit (HBTC) provides up to $1,500 in federal tax relief in the year of purchase. [3]

- CMHC mortgage insurance allows buyers to purchase with as little as 5% down on homes up to $1.5 million. [2]

- The mortgage stress test requires qualifying at the higher of 5.25% or your contract rate plus 2% — preparation matters.

- Closing costs in Ontario typically run 1.5% to 4% of the purchase price, beyond the down payment.

What Does "First Time Home Buyer" Actually Mean in Ontario?

In Ontario, a first time home buyer is generally someone who has never owned a residential property anywhere in the world. This definition applies to most federal and provincial programs, though the exact wording varies slightly by program.

Key eligibility points to know:

- Federal programs (FHSA, HBP, HBTC): You must be a Canadian resident and must not have lived in a home you or your spouse/common-law partner owned in the current year or the previous four calendar years.

- Ontario Land Transfer Tax Rebate: You must be a Canadian citizen or permanent resident, at least 18 years old, and the home must be your principal residence within 9 months of purchase.

- Toronto Municipal Rebate: Same basic criteria as the provincial rebate, but applies only to properties within Toronto city limits.

- Couples: If one partner has previously owned a home, only the other partner may qualify individually for certain rebates — this can reduce (but not eliminate) available benefits.

💡 Edge case: If you owned a home outside Canada in the past, you may still qualify for some Ontario programs. Always verify eligibility with a licensed mortgage professional before assuming you don't qualify.

What Programs Are Available for First Time Home Buyers in Ontario?

Ontario first time home buyers have access to a layered set of federal and provincial programs. Used together, these can meaningfully reduce both the upfront costs and the long-term tax burden of buying a home.

1. First Home Savings Account (FHSA)

The FHSA is one of the most valuable tools available. It's a registered account that lets eligible buyers contribute up to $8,000 per year, to a lifetime maximum of $40,000. [2] Contributions are tax-deductible (like an RRSP), and withdrawals for a qualifying home purchase are completely tax-free (like a TFSA).

- Unused contribution room carries forward one year.

- The account can be open for up to 15 years or until you turn 71.

- You can hold the FHSA alongside an RRSP and use both for the same purchase.

For a deeper breakdown, see this introduction to the First Home Savings Account and how it compares to other savings vehicles.

2. Home Buyers' Plan (HBP)

The HBP lets first-time buyers withdraw up to $60,000 per person (or $120,000 for a couple) from their RRSP to fund a home purchase, with no immediate tax consequence. [2] The withdrawn amount must be repaid to the RRSP over 15 years, starting two years after the withdrawal year.

- If you don't repay in a given year, that year's repayment amount is added to your taxable income.

- You can use both the HBP and FHSA for the same purchase.

For more on how this works in practice, read RRSPs and the Home Buyers' Plan: What You Need to Know.

3. Land Transfer Tax Rebates

Ontario charges a provincial land transfer tax on every home purchase. First-time buyers receive a rebate of up to $4,000, which effectively eliminates the tax on homes priced up to approximately $368,000. [3] For higher-priced homes, the rebate reduces but doesn't eliminate the tax.

Toronto buyers pay a second, municipal land transfer tax and receive an additional rebate of up to $4,475. [3] Combined, Toronto first-time buyers can receive up to $8,475 in land transfer tax relief.

4. First-Time Home Buyers' Tax Credit (HBTC)

This is a federal non-refundable tax credit worth up to $1,500 in the year you purchase a qualifying home. [3] It applies to a $10,000 amount at the 15% federal tax rate. It won't cover your full closing costs, but it's straightforward to claim on your tax return and requires no pre-registration.

For the full picture on claiming this credit, see the guide to the First Time Home Buyer Tax Credit in Canada.

5. CMHC Mortgage Insurance (Low Down Payment Purchases)

Buyers with less than 20% down are required to purchase mortgage default insurance through CMHC (or a private insurer). While this adds a premium to the mortgage, it allows buyers to enter the market with as little as 5% down on homes priced up to $1.5 million. [2]

| Down Payment | CMHC Premium (% of mortgage) |

|---|---|

| 5% to 9.99% | 4.00% |

| 10% to 14.99% | 3.10% |

| 15% to 19.99% | 2.80% |

Source: CMHC [8]

The premium is added to the mortgage balance, not paid upfront (though provincial sales tax on the premium is paid at closing).

How Much Do You Actually Need to Save Before Buying?

The down payment is only part of the picture. First time home buyers in Ontario need to budget for several upfront costs beyond the deposit.

Minimum down payment rules (as of 2026):

- Homes up to $500,000: 5% minimum

- Homes $500,000 to $1,499,999: 5% on the first $500,000 + 10% on the remainder

- Homes $1.5 million and above: 20% minimum (not CMHC-insurable)

Closing costs to budget for (beyond the down payment):

- Land transfer tax (provincial, and municipal if in Toronto): varies by price

- Legal fees and disbursements: typically $1,500 to $2,500

- Home inspection: $400 to $600 (estimated)

- Title insurance: $200 to $400 (estimated)

- Mortgage default insurance premium tax (Ontario): 8% of the CMHC premium, paid at closing

- Adjustments and prepaid costs: property tax and utility adjustments at closing

As a general rule, budget 1.5% to 4% of the purchase price for closing costs, on top of your down payment. For a $700,000 home, that's roughly $10,500 to $28,000 in additional costs.

For a detailed breakdown, the closing cost calculator guide for Toronto homebuyers walks through each line item.

How Does the Mortgage Stress Test Affect First Time Buyers?

The mortgage stress test is a federal rule requiring all buyers (not just first-timers) to qualify at a rate higher than their actual contract rate. Specifically, you must qualify at the higher of 5.25% or your contract rate plus 2%.

This means if you're offered a 5-year fixed rate of 4.5%, you must prove you can afford payments at 6.5%. The practical effect is that your maximum approved mortgage is lower than it would be without the stress test.

What this means for first-time buyers:

- You may qualify for less than you expect, especially if your income is moderate relative to Ontario home prices.

- Getting pre-approved before house hunting is essential — it sets a realistic budget.

- A co-signer or co-borrower can help increase the qualifying amount.

For a full breakdown of how this works, see the mortgage stress test for home buyers in Canada.

Choose pre-approval if: you're actively house hunting. Choose pre-qualification if you're still 6–12 months away from buying and just want a rough number.

For the full pre-approval process in Ontario, the ins and outs of mortgage pre-approval in Ontario is a useful starting point.

What Are the Step-by-Step Stages of Buying Your First Home in Ontario?

Buying a first home in Ontario follows a fairly consistent process, though timelines vary. Here's a practical overview:

Step 1: Assess your finances

- Check your credit score (aim for 680+ for best rates).

- Calculate your total savings: down payment + closing costs + emergency reserve.

- Open an FHSA if you haven't already — even a year of contributions helps.

Step 2: Get mortgage pre-approval

- Gather documents: T4s or NOAs, pay stubs, bank statements, ID.

- Apply through a mortgage broker or lender.

- Pre-approval locks in a rate for 90–120 days (typically).

Step 3: Define your search criteria

- Set a realistic price range based on pre-approval, not maximum qualification.

- Decide on property type: condo, townhouse, detached. For a comparison, see home purchase in Ontario: condo versus house.

- Choose target neighborhoods based on commute, schools, and resale potential.

Step 4: Work with a real estate agent

- A buyer's agent costs you nothing directly (seller pays commission in most cases).

- They provide access to MLS listings, market comparables, and offer negotiation support.

Step 5: Make an offer

- Include conditions: financing, home inspection, status certificate (for condos).

- Be prepared for multiple offer situations in competitive Ontario markets.

Step 6: Satisfy conditions and close

- Complete your home inspection.

- Finalize mortgage approval with your lender.

- Work with a real estate lawyer to review title, transfer funds, and register the deed.

- Receive keys on closing day.

Common mistake: Skipping the home inspection to win a bidding war. In a balanced or buyer's market (like much of Ontario in 2026), conditions are more accepted. Waiving inspection on a resale home carries real financial risk.

For a full walkthrough, the step-by-step guide to buying your first home in Toronto's 2026 buyers market covers the process in detail.

How Can First Time Home Buyers in Ontario Stack Programs to Maximize Savings?

Stacking multiple programs is legal and encouraged. Here's how a typical buyer might combine them:

Example scenario: A single buyer in Toronto purchasing a $650,000 condo in 2026.

| Program | Benefit |

|---|---|

| FHSA (2 years of contributions) | $16,000 tax-free savings + tax deduction |

| Home Buyers' Plan (RRSP withdrawal) | Up to $60,000 toward down payment |

| Ontario Land Transfer Tax Rebate | Up to $4,000 rebate |

| Toronto Municipal LTT Rebate | Up to $4,475 rebate |

| First-Time Home Buyers' Tax Credit | Up to $1,500 tax credit |

| Total potential benefit | ~$85,975+ |

Note: Actual savings depend on individual RRSP balances, FHSA contributions, and purchase price. Tax deduction values vary by marginal tax rate.

The key insight: each program targets a different cost. The FHSA and HBP reduce the down payment burden. The land transfer tax rebates reduce closing costs. The HBTC reduces your tax bill in the purchase year. Together, they address the three biggest financial barriers to entry. [3]

What Are the Biggest Mistakes First Time Buyers Make in Ontario?

Even well-prepared buyers make avoidable errors. The most common ones:

-

Underestimating closing costs. Many first-timers budget only for the down payment and are caught off guard by land transfer tax, legal fees, and adjustments.

-

Not opening an FHSA early enough. The FHSA requires the account to be open before a qualifying withdrawal. Even if you can't contribute much, opening the account early starts your contribution room clock.

-

Maxing out the mortgage qualification. Qualifying for $750,000 doesn't mean buying at $750,000 is comfortable. Leave room for property taxes, condo fees, maintenance, and life expenses.

-

Skipping mortgage rate comparison. Your bank's posted rate is rarely the best available. A mortgage broker compares rates across multiple lenders at no cost to you.

-

Ignoring the stress test impact on buying power. Many buyers are surprised when their pre-approval comes in lower than expected. Run the numbers before falling in love with a property.

For a fuller list, see first-time home buyer mistakes to avoid.

Is 2026 a Good Time for First Time Buyers to Enter the Ontario Market?

For many first-time buyers, 2026 presents a more accessible entry point than the peak years of 2021–2022. Market conditions across Ontario have moderated, with more inventory and less aggressive bidding in many segments.

Key factors working in buyers' favor in 2026:

- More balanced market conditions in many Ontario cities outside the core Toronto market.

- Rate environment: While rates remain higher than the historic lows of 2020–2021, the Bank of Canada has made several cuts since 2024, improving affordability relative to recent peaks.

- Extended amortizations: As of late 2024, 30-year amortizations became available for first-time buyers on new construction, reducing monthly payments.

- Condo market softness: In Toronto specifically, the condo segment has seen price corrections, creating opportunities for first-time buyers who are flexible on property type.

That said, timing the market perfectly is rarely possible. The more important question is whether your financial situation — savings, income stability, credit — is ready. A market dip means little if you're not in a position to qualify or sustain the costs of ownership.

For a current market perspective, see why 2026 may be the right entry point for first-time buyers in Toronto's cooling market.

FAQ: First Time Home Buyers Ontario

Q: Can I use both the FHSA and the Home Buyers' Plan for the same purchase?

Yes. You can withdraw from both your FHSA and your RRSP (via the HBP) for the same qualifying home purchase. This is one of the most effective ways to maximize your down payment savings. [2]

Q: What is the income limit for first-time buyer programs in Ontario?

Most federal programs (FHSA, HBP, HBTC) have no income cap. Eligibility is based on first-time buyer status, residency, and property type — not income level.

Q: Do I qualify as a first-time buyer if my spouse previously owned a home?

It depends on the program. For the Ontario Land Transfer Tax Rebate, if your spouse has previously owned a home, you will not receive the rebate even if this is your first purchase. For the FHSA and HBP, each person's eligibility is assessed individually.

Q: How long does it take to buy a home in Ontario from start to finish?

From starting your search to closing, most buyers take 3 to 6 months. The closing period itself (from accepted offer to key handover) is typically 30 to 90 days, depending on what's negotiated.

Q: Is a home inspection mandatory in Ontario?

No, a home inspection is not legally required. However, it is strongly recommended for resale properties. Skipping it to win a bidding war is a common mistake that can lead to costly surprises.

Q: What credit score do I need to get a mortgage in Ontario?

Most major lenders require a minimum credit score of 680 for the best rates. Scores between 600 and 679 may still qualify, but typically at higher rates or with a larger down payment. Scores below 600 may require alternative or private lending. See the guide to getting a mortgage with bad credit in Ontario.

Q: Can self-employed buyers access first-time buyer programs in Ontario?

Yes. Self-employed buyers qualify for the same programs as salaried employees, provided they meet the eligibility criteria. The mortgage qualification process may require additional documentation (e.g., two years of NOAs). See opportunities for first-time homebuyers among self-employed Canadians.

Q: What happens if I don't repay my Home Buyers' Plan withdrawal?

If you miss an annual repayment, that year's required repayment amount is added to your taxable income for that year. You don't lose the home, but you lose the tax-sheltered benefit on that portion of the withdrawal.

Q: Are new construction homes treated differently for first-time buyers?

Yes, in some ways. New builds may qualify for GST/HST rebates on the purchase price. As of late 2024, first-time buyers purchasing new construction can also access 30-year amortizations, which reduces monthly payments compared to the standard 25-year maximum for resale purchases with less than 20% down.

Q: What documents do I need to apply for a mortgage in Ontario?

Typically: government-issued ID, proof of income (T4s, pay stubs, or NOAs for self-employed), proof of down payment source (bank statements, FHSA/RRSP statements), and a signed purchase agreement. See the mortgage document checklist for a complete list.

Conclusion: Your Next Steps as a First Time Home Buyer in Ontario

Buying your first home in Ontario is one of the largest financial decisions you'll make, but the process is manageable when broken into clear steps. The programs available in 2026 — the FHSA, HBP, land transfer tax rebates, and the HBTC — can collectively save eligible buyers tens of thousands of dollars when used together. [2][3]

Actionable next steps:

- Open an FHSA today if you haven't already. Even if you're 2–3 years from buying, contribution room accumulates and every dollar saved tax-free matters.

- Check your RRSP balance and understand how much you could access through the Home Buyers' Plan.

- Pull your credit report and address any issues before applying for a mortgage.

- Get a mortgage pre-approval so you know your real budget before falling in love with a property.

- Work with a mortgage broker who can compare rates across lenders and help you stack programs effectively.

- Budget for closing costs, not just the down payment. A realistic total cost picture prevents last-minute surprises.

The Ontario housing market in 2026 offers first-time buyers more breathing room than in recent years. The programs are there, the market has moderated, and the tools to prepare have never been more accessible. The best move is to start now, even if the purchase is still months away.

References

[2] First Time Home Buyer Programs Incentives For Toronto Home Buyers – https://www.elevatepartners.ca/resources/first-time-home-buyer-programs-incentives-for-toronto-home-buyers/

[3] First Time Home Buyer Incentives – https://bridge.broker/real-estate-investment/first-time-home-buyer-incentives/

[5] First Time Homebuyer Incentives In Canada – https://blog.remax.ca/first-time-homebuyer-incentives-in-canada/

[7] First Time Home Buyer Canada – https://wowa.ca/calculators/first-time-home-buyer-canada

[8] First Time Home Buyer Incentive – https://www.cmhc-schl.gc.ca/consumers/home-buying/first-time-home-buyer-incentive

Tags: first time home buyers ontario, FHSA, Home Buyers Plan, land transfer tax rebate, CMHC mortgage insurance, mortgage stress test, Ontario housing market, first time home buyer programs, mortgage pre-approval, home buying steps ontario, first home savings account, HBTC tax credit